- In 50 of the country’s 100 largest cities, single people need 2 to 9 decades to save up enough to cover the difference between what the bank will lend them and the price of a starter home.

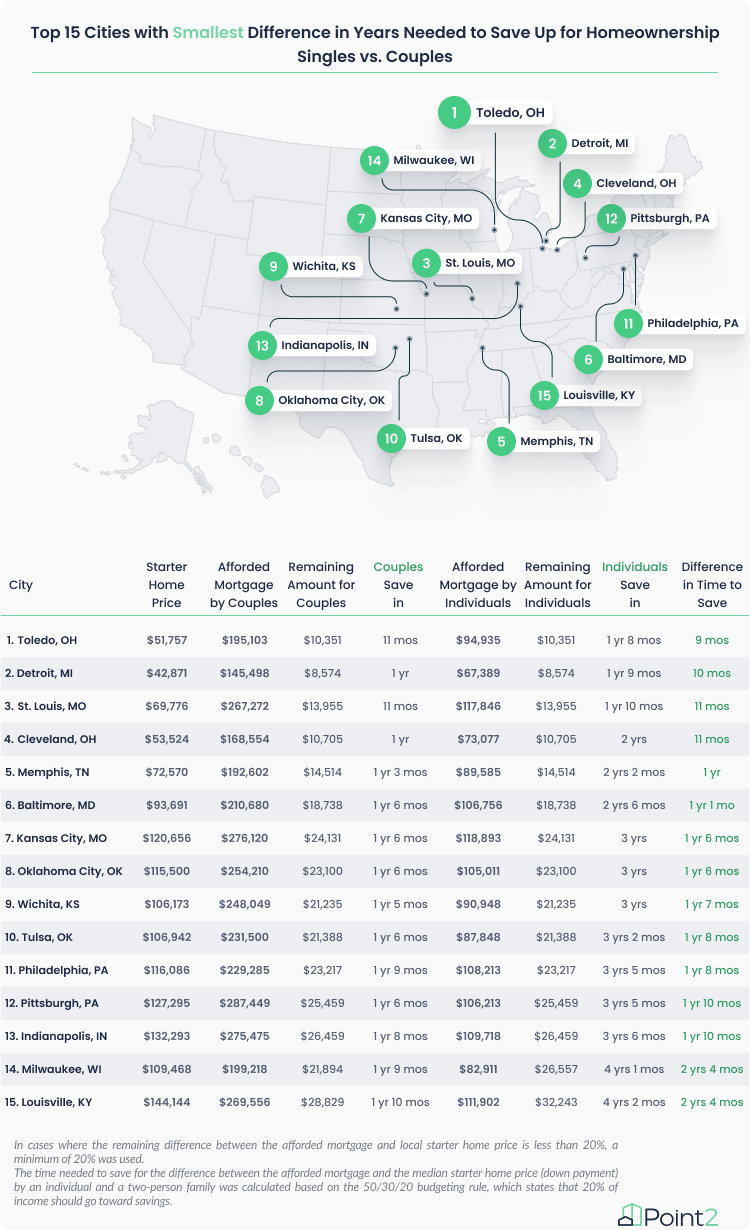

- In 5 cities, individuals would require just a few more months than couples to save up and become homeowners: Buying solo in Ohio’s Toledo and Cleveland, Detroit, MI, St. Louis, MO, and Memphis, TN wouldn’t take much longer than buying together.

- Singles in 13 major cities — including Philadelphia, PA, Indianapolis, IN, and Baltimore, MD — could afford a mortgage equal to at least 80% of the local starter home price. Couples have this chance in 79 out of 100 cities.

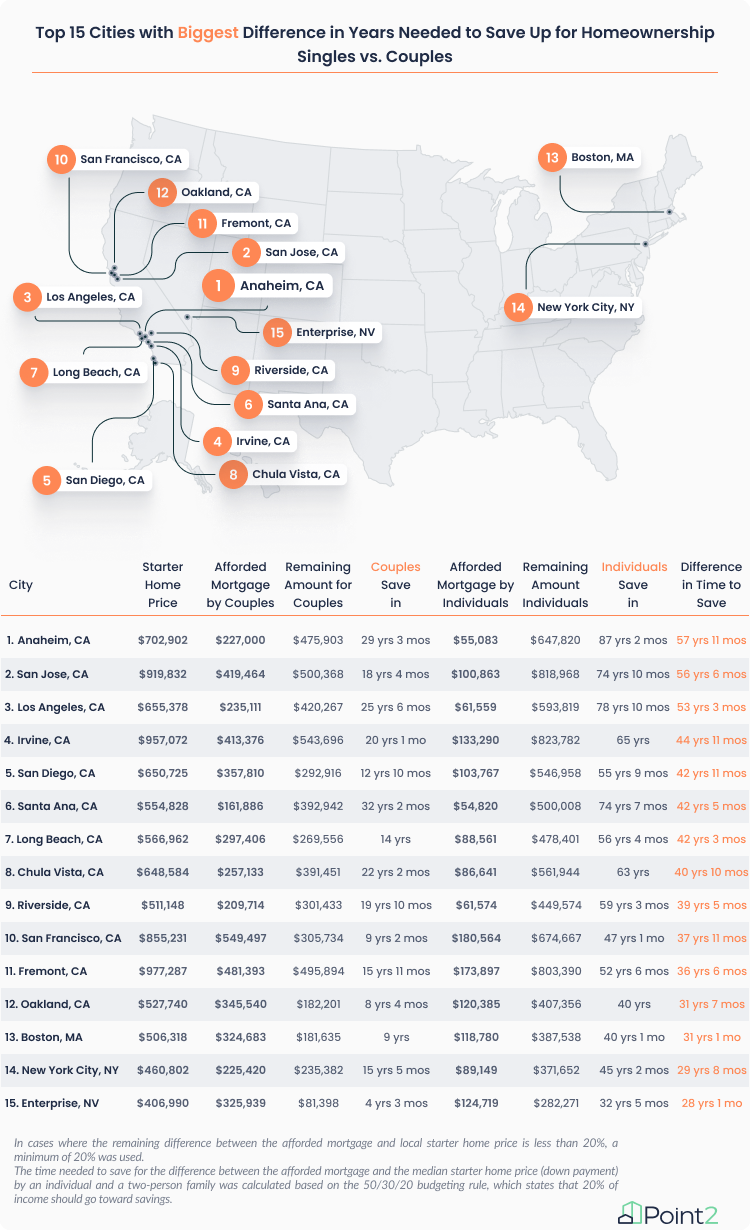

- It’s hard to see homebuying through heart-shaped glasses in California, but relationship status might make a lifetime of difference in savings. With a partner, it can take around 30 years to comfortably bridge the gap between an affordable loan and the cost of a starter home. Doing it alone can take a daunting 50 years more.

Single people don’t need to be reminded of the perks of having a significant other — especially during the month of love. But, they’d be happy to know that those perks aren’t automatically financial. In a few select cities in the Midwest, saving up to buy that first home can be almost as swift for singles as it is for couples — give or take a few months.

Solo, single, self-partnered… whatever the label, this cohort has had it rough in a housing market defined by sky-high prices, scarce inventory, and the almost-extinct concept of a starter home. With the median starter home price more than doubling in the past 20 years, singles in America’s major cities might take around 6 years more than couples to set money aside for an entry-level home.

Diligently saving up to cover what a bank loan doesn’t is a strenuous financial effort — particularly for those budgeting on their own.

With that in mind, and based on the incomes of individuals and couples, Point2Homes determined the maximum afforded mortgage (so that the monthly loan payment, taxes, and homeowners’ insurance wouldn't exceed 30% of their respective earnings). Next, we calculated the difference between the price of a starter home and the afforded loan to determine the remaining amount they would need to come up with for the down payment. Then, using the 50/30/20 budgeting rule, we discovered how much time it would take an individual to comfortably save up and cover the remaining amount compared to a couple in the same city.

In the Same Love Boat: Saving Up in the Midwest Is Fastest for Both Singles & Couples

Single homebuyers in 13 cities could afford an 80% mortgage, need just a few more months than couples to save up for the remaining amount

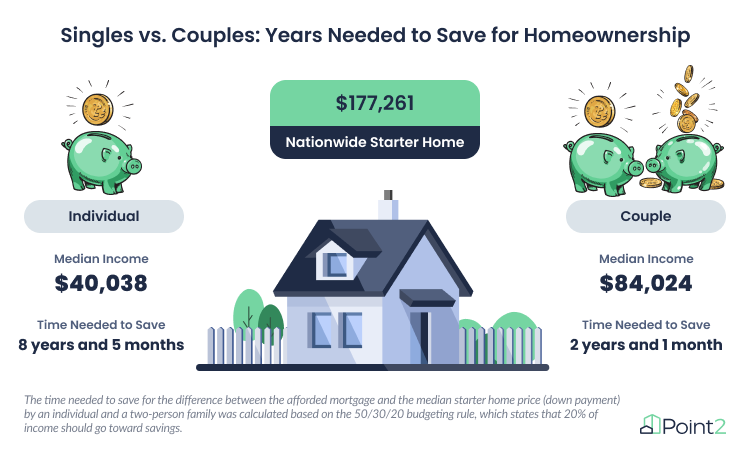

We already know that single people, especially in big cities, need years and years more than couples to set money aside for an entry-level home. Specifically, the nationwide average to bridge the gap between an affordable loan and the $177,260 starter home price is 2 years for a couple and 8 and a half years for single people.

So, when analyzing how the journey to homeownership differs for singles and couples, it’s mathematically easier in two. In half of the country’s major cities, a couple in want of an affordable mortgage that won't eat up more than 30% of their combined income can pool resources and save up to cover the remaining amount in 3 years or less.

However, a partner would not significantly boost homeownership savings in other cities — particularly in the more reasonably priced Midwest, where starter home prices are a portion of the national median. In one-third of the country's major cities, individuals can afford a mortgage equal to more than half of the local starter home price. And, in 13 of them, a single person can afford an 80% mortgage, meaning that one can budget and save for the remaining amount in 3 years and 6 months or less.

Going by the 50/30/20 rule, in Toledo, OH, Detroit, MI, St. Louis, MO, and Cleveland, OH, a single person might require just 9 to 11 months more than a two-person family to set money aside. To cover the difference between a bank loan and the price of a starter home in Memphis, TN, Baltimore, MD, Kansas City, MO, or Oklahoma City, OK, single homebuyers would need to save up 1 year to 1 year and a half more than couples in the same cities.

These are the same cities where individuals on their own would need the least amount of time to save up to become homeowners: Less than 2 years in Toledo, Detroit, and St. Louis, and 2 to 3 years in Memphis, Baltimore, Kansas City, and Oklahoma City, as well as in Cleveland and Wichita, KS.

An Affordable Loan in California, a Lifetime of Saving Up for Homeownership

In 8 cities, setting aside 20% of income puts single people 40+ years behind couples

Of course, local market dynamics play a huge role in assessing someone’s track to homebuying. For instance, an individual in Arlington, VA makes twice as much as a couple in Laredo, TX. However, a single person with an affordable mortgage in Arlington needs more than 8 years to set aside the $146,600 still to go on a $409,700 starter home. On the other hand, a Laredo couple can do so in half the time to cover the $39,440 they need for a $137,200 entry-level home.

And, if the Midwest and Southeast can give hope to solo homebuyers, single people need all the help they can get in California:

Major markets in the Golden State don’t agree with single first-time homebuyers. Fresno is the fastest large city here to set aside money on one’s own, but it’s still a doozy — It can take more than two decades to set aside 20% of the $33,500 median income and cover the smallest remaining difference for an individual in a major California city.

Meanwhile, the slowest city to save in as a single person is Anaheim — a city where an affordable mortgage for an individual is just 8% of the starter home price. This means that the remaining amount that one must set aside represents a significant portion of the $702,900 cost of an entry-level home. Hypothetically, this means that saving up in the home of the Disneyland Resort can take one person more than 87 years — Nearly 6 decades more than it takes a couple pooling their savings monthly.

Similarly, single homebuyers in San Jose are just as ill-fated when going by the 50/30/20 rule: With the mortgage covering just 11% of the $920,000 starter home price, it could take them nearly 75 years to set aside 20% of their income to cover the disheartening $819,000 amount still needed.

Despite the surprisingly smaller starter home price, buying solo in Los Angeles is about as difficult as you'd expect: Covering the entire amount left after the maximum affordable loan from the bank means budgeting 5 decades more than a couple.

While buying a home together is traditionally associated with romantic couples, the dire state of the housing market has led to a rise in non-romantic homebuying partnerships. The reason behind it is the same: Two incomes mean saving faster, while also enhancing the chances for mortgage approval. But it also draws the need for a bigger, pricier home.

In the least affordable housing market since the early 1980s, purchasing a home has become decidedly influenced by economic factors. Big life decisions — such as starting a family or choosing to live one’s best single life — take a backseat as budgeting resources becomes a priority that resonates with everyone.

Check out the savings gap between singles and couples looking to cover the difference between the maximum mortgage afforded and the median starter home price in the country’s 100 largest cities:

| City, State | Starter Home Price | Median Income for Couples | Afforded Mortgage by Couples | Remaining Amount for Couples | Years Couples Need to Save In | Median Income for Individuals | Afforded Mortgage by Individuals | Remaining Amount for Individuals | Years Individuals Need to Save In | Difference in Years to Save |

|---|---|---|---|---|---|---|---|---|---|---|

| Toledo, OH | $51,757 | $57,573 | $195,103 | $10,351 | 0.9 | $31,825 | $94,935 | $10,351 | 1.6 | 0.73 |

| Detroit, MI | $42,871 | $44,196 | $145,498 | $8,574 | 1.0 | $24,118 | $67,389 | $8,574 | 1.8 | 0.81 |

| St. Louis, MO | $69,776 | $76,221 | $267,272 | $13,955 | 0.9 | $37,811 | $117,846 | $13,955 | 1.8 | 0.93 |

| Cleveland, OH | $53,524 | $51,524 | $168,554 | $10,705 | 1.0 | $26,982 | $73,077 | $10,705 | 2.0 | 0.94 |

| Memphis, TN | $72,570 | $59,492 | $192,602 | $14,514 | 1.2 | $33,012 | $89,585 | $14,514 | 2.2 | 0.98 |

| Baltimore, MD | $93,691 | $64,069 | $210,680 | $18,738 | 1.5 | $37,355 | $106,756 | $18,738 | 2.5 | 1.05 |

| Kansas City, MO | $120,656 | $81,085 | $276,120 | $24,131 | 1.5 | $40,670 | $118,893 | $24,131 | 3.0 | 1.48 |

| Oklahoma City, OK | $115,500 | $77,103 | $254,210 | $23,100 | 1.5 | $38,751 | $105,011 | $23,100 | 3.0 | 1.48 |

| Wichita, KS | $106,173 | $75,957 | $248,049 | $21,235 | 1.4 | $35,574 | $90,948 | $21,235 | 3.0 | 1.59 |

| Tulsa, OK | $106,942 | $71,100 | $231,500 | $21,388 | 1.5 | $34,174 | $87,848 | $21,388 | 3.1 | 1.63 |

| Philadelphia, PA | $116,086 | $65,054 | $229,285 | $23,217 | 1.8 | $33,932 | $108,213 | $23,217 | 3.4 | 1.64 |

| Indianapolis, IN | $132,293 | $80,265 | $275,475 | $26,459 | 1.6 | $37,657 | $109,718 | $26,459 | 3.5 | 1.86 |

| Pittsburgh, PA | $127,295 | $84,264 | $287,449 | $25,459 | 1.5 | $37,677 | $106,213 | $25,459 | 3.4 | 1.87 |

| Milwaukee, WI | $109,468 | $62,548 | $199,218 | $21,894 | 1.8 | $32,651 | $82,911 | $26,557 | 4.1 | 2.32 |

| Louisville, KY | $144,144 | $78,950 | $269,556 | $28,829 | 1.8 | $38,425 | $111,902 | $32,243 | 4.2 | 2.37 |

| Fort Wayne, IN | $133,747 | $73,742 | $252,163 | $26,749 | 1.8 | $35,053 | $101,650 | $32,096 | 4.6 | 2.76 |

| Columbus, OH | $152,097 | $76,526 | $246,096 | $30,419 | 2.0 | $38,805 | $99,347 | $52,750 | 6.8 | 4.81 |

| Chicago, IL | $162,091 | $81,952 | $250,556 | $32,418 | 2.0 | $42,386 | $96,633 | $65,457 | 7.7 | 5.74 |

| Atlanta, GA | $236,744 | $110,237 | $381,956 | $47,349 | 2.1 | $51,439 | $153,217 | $83,527 | 8.1 | 5.97 |

| Corpus Christi, TX | $123,810 | $63,642 | $184,888 | $24,762 | 1.9 | $33,932 | $69,309 | $54,500 | 8.0 | 6.09 |

| Arlington, VA | $409,677 | $184,671 | $649,023 | $81,935 | 2.2 | $85,459 | $263,060 | $146,617 | 8.6 | 6.36 |

| New Orleans, LA | $143,664 | $67,301 | $220,895 | $28,733 | 2.1 | $32,654 | $86,110 | $57,554 | 8.8 | 6.68 |

| Winston-Salem, NC | $146,952 | $70,202 | $231,090 | $29,390 | 2.1 | $32,942 | $86,136 | $60,817 | 9.2 | 7.14 |

| Lubbock, TX | $126,937 | $76,376 | $235,483 | $25,387 | 1.7 | $32,978 | $66,655 | $60,283 | 9.1 | 7.48 |

| Anchorage, AK | $245,669 | $110,123 | $368,440 | $49,134 | 2.2 | $51,477 | $140,290 | $105,378 | 10.2 | 8.00 |

| Washington, D.C. | $376,860 | $142,348 | $513,003 | $75,372 | 2.6 | $69,083 | $227,981 | $148,879 | 10.8 | 8.13 |

| Jacksonville, FL | $185,908 | $77,606 | $252,061 | $37,182 | 2.4 | $39,028 | $101,984 | $83,924 | 10.8 | 8.36 |

| Cincinnati, OH | $148,505 | $76,841 | $249,517 | $29,701 | 1.9 | $33,195 | $79,720 | $68,785 | 10.4 | 8.43 |

| Minneapolis, MN | $209,058 | $116,655 | $392,155 | $41,812 | 1.8 | $44,693 | $112,204 | $96,854 | 10.8 | 9.04 |

| Greensboro, NC | $154,290 | $76,355 | $253,292 | $30,858 | 2.0 | $32,304 | $81,921 | $72,370 | 11.2 | 9.18 |

| Lexington, KY | $198,140 | $83,528 | $280,411 | $39,628 | 2.4 | $38,116 | $103,745 | $94,395 | 12.4 | 10.01 |

| Buffalo, NY | $141,994 | $58,101 | $162,923 | $28,399 | 2.4 | $31,887 | $60,944 | $81,050 | 12.7 | 10.26 |

| Omaha, NE | $178,876 | $87,246 | $262,193 | $35,775 | 2.1 | $40,043 | $78,561 | $100,315 | 12.5 | 10.48 |

| Chesapeake, VA | $262,534 | $90,099 | $301,704 | $52,507 | 2.9 | $46,206 | $130,947 | $131,588 | 14.2 | 11.33 |

| Dallas, TX | $190,497 | $74,409 | $211,927 | $38,099 | 2.6 | $39,372 | $75,624 | $114,873 | 14.6 | 12.03 |

| St. Paul, MN | $208,768 | $84,543 | $265,381 | $41,754 | 2.5 | $39,859 | $91,547 | $117,221 | 14.7 | 12.24 |

| Richmond, VA | $225,286 | $87,348 | $295,250 | $45,057 | 2.6 | $39,115 | $107,609 | $117,677 | 15.0 | 12.46 |

| Virginia Beach, VA | $277,443 | $94,723 | $319,672 | $55,489 | 2.9 | $46,265 | $131,156 | $146,287 | 15.8 | 12.88 |

| Laredo, TX | $137,225 | $43,090 | $97,785 | $39,440 | 4.6 | $27,915 | $38,749 | $98,476 | 17.6 | 13.06 |

| St. Petersburg, FL | $243,635 | $93,538 | $309,664 | $48,727 | 2.6 | $42,367 | $110,597 | $133,038 | 15.7 | 13.10 |

| Fort Worth, TX | $203,241 | $81,132 | $232,190 | $40,648 | 2.5 | $40,176 | $72,859 | $130,382 | 16.2 | 13.72 |

| Houston, TX | $182,690 | $71,143 | $198,682 | $36,538 | 2.6 | $35,531 | $60,141 | $122,549 | 17.2 | 14.68 |

| San Antonio, TX | $167,563 | $66,412 | $182,285 | $33,513 | 2.5 | $33,163 | $52,941 | $114,623 | 17.3 | 14.76 |

| Charlotte, NC | $284,386 | $85,267 | $275,180 | $56,877 | 3.3 | $45,316 | $119,760 | $164,626 | 18.2 | 14.83 |

| Lincoln, NE | $193,408 | $78,929 | $230,522 | $38,682 | 2.5 | $36,349 | $64,872 | $128,536 | 17.7 | 15.23 |

| Madison, WI | $256,517 | $103,479 | $328,467 | $51,303 | 2.5 | $43,954 | $96,899 | $159,618 | 18.2 | 15.68 |

| Norfolk, VA | $208,819 | $78,626 | $259,554 | $41,764 | 2.7 | $33,641 | $84,553 | $124,266 | 18.5 | 15.81 |

| Tampa, FL | $249,562 | $91,541 | $297,390 | $49,912 | 2.7 | $40,397 | $98,425 | $151,137 | 18.7 | 15.98 |

| Albuquerque, NM | $246,457 | $78,316 | $253,686 | $49,291 | 3.1 | $38,519 | $98,864 | $147,593 | 19.2 | 16.01 |

| Durham, NC | $284,431 | $95,040 | $308,399 | $56,886 | 3.0 | $44,484 | $111,724 | $172,707 | 19.4 | 16.42 |

| Orlando, FL | $250,078 | $76,244 | $239,116 | $50,016 | 3.3 | $38,458 | $92,119 | $157,959 | 20.5 | 17.26 |

| Raleigh, NC | $310,300 | $94,531 | $311,416 | $62,060 | 3.3 | $45,393 | $120,255 | $190,045 | 20.9 | 17.65 |

| Denver, CO | $380,514 | $112,724 | $372,745 | $76,103 | 3.4 | $54,363 | $145,703 | $234,811 | 21.6 | 18.22 |

| Nashville, TN | $306,910 | $90,261 | $297,401 | $61,382 | 3.4 | $43,893 | $117,016 | $189,895 | 21.6 | 18.23 |

| El Paso, TX | $161,657 | $56,095 | $136,966 | $32,331 | 2.9 | $29,569 | $33,775 | $127,883 | 21.6 | 18.74 |

| Phoenix, AZ | $316,234 | $86,328 | $291,616 | $63,247 | 3.7 | $42,755 | $122,103 | $194,131 | 22.7 | 19.04 |

| Spokane, WA | $272,383 | $82,373 | $268,678 | $54,477 | 3.3 | $38,243 | $97,001 | $175,382 | 22.9 | 19.62 |

| Irving, TX | $254,053 | $85,867 | $241,584 | $50,811 | 3.0 | $40,645 | $65,659 | $188,394 | 23.2 | 20.22 |

| Scottsdale, AZ | $453,009 | $125,017 | $432,015 | $90,602 | 3.6 | $58,347 | $172,650 | $280,359 | 24.0 | 20.40 |

| Henderson, NV | $348,006 | $93,264 | $322,319 | $69,601 | 3.7 | $44,264 | $131,692 | $216,314 | 24.4 | 20.70 |

| Chandler, AZ | $406,857 | $101,402 | $343,559 | $81,371 | 4.0 | $51,805 | $150,612 | $256,245 | 24.7 | 20.72 |

| Las Vegas, NV | $292,647 | $77,480 | $265,006 | $58,529 | 3.8 | $37,381 | $109,008 | $183,639 | 24.6 | 20.79 |

| Garland, TX | $236,102 | $72,415 | $193,463 | $47,220 | 3.3 | $37,242 | $56,631 | $179,471 | 24.1 | 20.83 |

| Mesa, AZ | $332,378 | $86,100 | $289,535 | $66,476 | 3.9 | $42,089 | $118,318 | $214,060 | 25.4 | 21.57 |

| Jersey City, NJ | $402,168 | $110,983 | $305,173 | $96,995 | 4.4 | $57,351 | $96,531 | $305,637 | 26.6 | 22.28 |

| Tucson, AZ | $245,661 | $68,448 | $216,760 | $49,132 | 3.6 | $32,476 | $76,819 | $168,842 | 26.0 | 22.41 |

| North Las Vegas, NV | $319,910 | $74,797 | $252,554 | $67,356 | 4.5 | $38,421 | $111,038 | $208,872 | 27.2 | 22.68 |

| Austin, TX | $373,010 | $125,139 | $368,377 | $74,602 | 3.0 | $54,065 | $91,877 | $281,133 | 26.0 | 23.02 |

| Colorado Springs, CO | $347,594 | $95,529 | $314,144 | $69,519 | 3.6 | $43,742 | $112,677 | $234,917 | 26.9 | 23.21 |

| Plano, TX | $379,118 | $110,573 | $305,391 | $75,824 | 3.4 | $54,434 | $86,995 | $292,123 | 26.8 | 23.40 |

| Gilbert, AZ | $460,461 | $109,889 | $372,611 | $92,092 | 4.2 | $54,726 | $158,011 | $302,450 | 27.6 | 23.44 |

| Seattle, WA | $560,314 | $154,767 | $519,889 | $112,063 | 3.6 | $68,941 | $186,000 | $374,314 | 27.1 | 23.53 |

| Arlington, TX | $251,023 | $83,051 | $227,760 | $50,205 | 3.0 | $37,512 | $50,598 | $200,425 | 26.7 | 23.69 |

| Fresno, CA | $263,195 | $71,491 | $226,325 | $52,639 | 3.7 | $33,494 | $78,506 | $184,689 | 27.6 | 23.89 |

| Stockton, CA | $333,551 | $68,853 | $208,148 | $125,403 | 9.1 | $37,064 | $84,480 | $249,071 | 33.6 | 24.49 |

| Newark, NJ | $340,097 | $47,010 | $74,889 | $265,208 | 28.2 | $30,939 | $12,366 | $327,732 | 53.0 | 24.76 |

| Portland, OR | $381,817 | $110,755 | $368,028 | $76,363 | 3.4 | $46,237 | $117,038 | $264,779 | 28.6 | 25.19 |

| Honolulu, HI | $408,009 | $93,891 | $336,630 | $81,602 | 4.3 | $43,997 | $142,527 | $265,481 | 30.2 | 25.82 |

| Glendale, AZ | $324,232 | $82,307 | $275,378 | $64,846 | 3.9 | $37,328 | $100,397 | $223,835 | 30.0 | 26.04 |

| Miami, FL | $365,138 | $57,017 | $151,040 | $214,098 | 18.8 | $33,844 | $60,890 | $304,248 | 44.9 | 26.17 |

| Aurora, CO | $358,958 | $91,383 | $291,314 | $71,792 | 3.9 | $42,692 | $101,895 | $257,063 | 30.1 | 26.18 |

| Boise City, ID | $374,078 | $94,567 | $318,154 | $74,816 | 4.0 | $41,955 | $113,480 | $260,598 | 31.1 | 27.10 |

| Sacramento, CA | $368,393 | $98,596 | $320,585 | $73,679 | 3.7 | $42,446 | $102,144 | $266,249 | 31.4 | 27.63 |

| Reno, NV | $374,814 | $86,097 | $295,371 | $79,443 | 4.6 | $40,007 | $116,069 | $258,745 | 32.3 | 27.72 |

| Bakersfield, CA | $283,444 | $76,721 | $237,167 | $56,689 | 3.7 | $33,795 | $70,173 | $213,270 | 31.6 | 27.86 |

| Enterprise, NV | $406,990 | $95,316 | $325,939 | $81,398 | 4.3 | $43,592 | $124,719 | $282,271 | 32.4 | 28.11 |

| New York City, NY | $460,802 | $76,181 | $225,420 | $235,382 | 15.4 | $41,153 | $89,149 | $371,652 | 45.2 | 29.71 |

| Boston, MA | $506,318 | $101,265 | $324,683 | $181,635 | 9.0 | $48,338 | $118,780 | $387,538 | 40.1 | 31.12 |

| Oakland, CA | $527,740 | $108,838 | $345,540 | $182,201 | 8.4 | $50,962 | $120,385 | $407,356 | 40.0 | 31.60 |

| Fremont, CA | $977,287 | $155,598 | $481,393 | $495,894 | 15.9 | $76,556 | $173,897 | $803,390 | 52.5 | 36.54 |

| San Francisco, CA | $855,231 | $166,469 | $549,497 | $305,734 | 9.2 | $71,634 | $180,564 | $674,667 | 47.1 | 37.91 |

| Riverside, CA | $511,148 | $76,043 | $209,714 | $301,433 | 19.8 | $37,964 | $61,574 | $449,574 | 59.2 | 39.39 |

| Chula Vista, CA | $648,584 | $88,431 | $257,133 | $391,451 | 22.1 | $44,606 | $86,641 | $561,944 | 63.0 | 40.86 |

| Long Beach, CA | $566,962 | $96,176 | $297,406 | $269,556 | 14.0 | $42,492 | $88,561 | $478,401 | 56.3 | 42.28 |

| Santa Ana, CA | $554,828 | $61,049 | $161,886 | $392,942 | 32.2 | $33,527 | $54,820 | $500,008 | 74.6 | 42.38 |

| San Diego, CA | $650,725 | $114,363 | $357,810 | $292,916 | 12.8 | $49,062 | $103,767 | $546,958 | 55.7 | 42.94 |

| Irvine, CA | $957,072 | $135,348 | $413,376 | $543,696 | 20.1 | $63,352 | $133,290 | $823,782 | 65.0 | 44.93 |

| Los Angeles, CA | $655,378 | $82,285 | $235,111 | $420,267 | 25.5 | $37,673 | $61,559 | $593,819 | 78.8 | 53.28 |

| San Jose, CA | $919,832 | $136,633 | $419,464 | $500,368 | 18.3 | $54,736 | $100,863 | $818,968 | 74.8 | 56.50 |

| Anaheim, CA | $702,902 | $81,340 | $227,000 | $475,903 | 29.3 | $37,149 | $55,083 | $647,820 | 87.2 | 57.94 |

Methodology

Point2Homes, a division of Yardi Systems Inc., covers real estate trends and news. Point2Homes studies are based on internal data, public records, governmental sources, online research, and other reliable third-party agencies.

- For this study, we took into consideration the 100 largest U.S. cities, according to the most recent population data from the U.S. Census Bureau.

- Median income for individuals (aged 15 and older) and couples (2-person families) was sourced from the 2022 ACS 1-year estimates and adjusted for 2023 using the BLS Wages and salaries increase.

- We calculated the mortgage amount that an individual and a couple would be eligible for based on their respective incomes, assuming a monthly mortgage payment (including insurance and taxes) that doesn’t represent more than 30% of the median income and taking into consideration the 6.6%, 30-year fixed-rate mortgage as per FRED.

- We then calculated the difference between the maximum mortgage and local starter home price (also referred to as a down payment) needed to save to purchase a starter home. In cases where the down payment was less than 20% of the starter home price, we defaulted to a minimum of 20%.

- We used the 50/30/20 rule (where 20% of the income should go towards savings) to calculate and compare the years required to save up for a down payment by both individuals and couples.

- Tax rates sourced from SmartAsset; Homeowners Insurance values sourced from ValuePenguin.

- Median starter home prices as per Zillow. The study considers “starter homes” as those valued in the bottom one-third of a given region — that is, homes that fell within the 5th to 35th percentile range. For Enterprise, NV, the study uses an estimated median value for a starter home, based on active listings on the market.

Fair use and redistribution

We encourage and freely grant permission to reuse, host or repost this article. When doing so, we only ask that you kindly attribute the authors by linking to Point2Homes.com or this page, so that your readers can learn more about this project, the research behind it and its methodology.