BTR SFR Reports

Stay up-to-date with the latest trends in the build-to-rent single-family rental market through the monthly Point2Homes Build-to-Rent Single-Family Homes Market Reports backed by Yardi Matrix data.

BTR SFR Report – November 2025

BTR SFR Report: Miami Leads Occupancy as National Rents Hold Steady in November

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

November SFR Market Insights:

- National SFR occupancy held steady at 95%, maintaining the consistent levels observed in recent months.

- Asking rents for single-family build-to-rent homes averaged $2,185 in November, edging down $10 (or -0.5%) from the previous month.

National SFR conditions in November reflect a steady environment, with high occupancy continuing to track and rents edging down slightly from recent peaks.

The latest Yardi Matrix report points to strong annual increases in the Twin Cities and Chicago (both +7.9%), while the largest drops appeared in Austin (-3.9%), Charleston (-3.8%) and Pensacola (-2.5%). Although some seasonal softening is typical for this time of year, patterns remain mixed, with rent decreases concentrated in the Sun Belt while many Midwestern markets continue to post year-over-year gains.

The distribution, however, is balanced, with a similar number of markets recording flat or positive rent growth as those experiencing declines.

Multiple Major Markets with Occupancy Rates Over the 95% National Average

National SFR occupancy was 95% in November, in line with the pattern seen throughout the year. Several markets continue to outperform the national benchmark, with Miami Metro leading at 98%, followed by Chicago, Indianapolis, and Grand Rapids — each with occupancy at over 97%.

Among yearly changes, Jacksonville posted the strongest occupancy increase at 3.7%, followed by Miami Metro (+3.5%). Increases remained moderate across most markets, consistent with a sector where stabilized occupancy has been the norm for some time.

Asking Rents Show Selective Declines

While national rents averaged $2,185 in November, 17 markets posted asking rent prices below this mark. As many continue to move independently based on supply additions and leasing momentum, several experienced yearly decreases, which reflect localized adjustments rather than broad national trends.

Pensacola (-2.5%), Charleston (-3.8%), and Austin (-3.9%) recorded the biggest annual rent contractions. Other markets with y-o-y drops in asking rent prices are Dallas–Fort Worth, Miami Metro, Atlanta, and Phoenix.

In fact, Miami Metro is among the rent leaders, posting the highest average SFR asking price at $3,239, followed by the Inland Empire. These areas tend to rank among the highest-priced SFR markets, supported by sustained demand and strong absorption patterns.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – October 2025

In October, SFR Occupancy Stays Strong Despite Uneven Rent Growth Across Major Metros

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

October SFR Market Insights:

- Occupancy remained robust heading into the fall: U.S. single-family rental occupancy rose to 95.1% in October, up 10 basis points year-over-year.

- Renter-By-Necessity assets continued to outperform with a 96.4% occupancy rate, while Lifestyle-oriented properties posted a solid 94.9%.

- Nationally, asking rents for single-family build-to-rent homes slipped slightly in October, declining $6 to $2,195, but remained flat compared to the same period last year.

While national SFR occupancy has leveled off in recent months, regional performance in October shows some significant differences. The latest Yardi Matrix data highlights Jacksonville, Miami, Austin and Charleston as standout markets, each posting strong year-over-year occupancy gains, possibly driven by consistent in-migration and a slowdown in new supply.

In contrast, Nashville, Kansas City and Las Vegas recorded slight declines. Taken together, the trends suggest that stabilized occupancy levels are likely to hold through Q4 2025, even as developers continue to slow the pace of new starts.

Rent growth across BTR markets remains uneven. Among the Matrix Top 30 metros, 16 recorded year-over-year rent increases while 14 saw declines. The Midwest led the charge, representing seven of the nine strongest markets, headlined by the Twin Cities and Chicago (both up 7.0%) and Grand Rapids (up 5.4%).

At the other end of the spectrum, several large Sun Belt and Southeast metros posted the weakest rent performance in October. Austin led declines at –4.2% year-over-year, followed by Jacksonville (–1.9%), Nashville (–1.3%), Dallas (–1.0%), Las Vegas (–0.8%) and Miami (–0.7%).

These markets are grappling with elevated multifamily deliveries and softer for-sale dynamics where sellers outnumber buyers, particularly in Texas and Florida. Adding to the pressure is a growing cohort of “accidental landlords,” meaning homeowners opting to rent out properties rather than sell in order to preserve low mortgage rates or avoid competing in oversupplied for-sale markets. Their entry is creating unexpected competition for institutional SFR operators.

For renters, however, the shift offers a modest advantage. The influx of owner-leased homes is nudging single-family rental inventory higher, giving tenants slightly more leverage on asking rents. In several Sun Belt metros like Atlanta, Phoenix, Dallas, Houston and Tampa, inventory growth has surged by more than 20% over the past year, according to CNBC, meaning supply pressures are substantial enough to influence local rent trajectories.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – September 2025

SFR Occupancy Holds Steady as September Rent Growth Hits Decade Low

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

September SFR Market Insights:

- National occupancy remained firm at 95.1% in September, holding steady from last year and signaling that tenant demand continues to support stability across most markets.

- SFR rent rates experienced the sharpest monthly decline in a decade, dropping by $15 to bring the average to $2,194.

The single-family build-to-rent (SFR BTR) segment remained stable in September, with occupancy rates showing resilience as rent growth continued to soften. As demand continued in this cooling rent environment, national SFR occupancy held at 95.1% in September, virtually unchanged from last year.

While 2025 has marked a transition year for the SFR sector, fundamentals remain intact. Stable occupancy levels and a moderating pipeline of new completions point toward balanced conditions heading into 2026. Rent growth may remain muted in the short term, but with ongoing barriers to homeownership and constrained inventory, demand for build-to-rent housing is expected to stay solid across most markets.

Occupancy Rates Steady at 95%, Nearly Unchanged Year-Over-Year

Although SFR occupancy rates have plateaued in recent months, regional performance continues to vary in September. According to the September Yardi Matrix report, markets such as Jacksonville, Miami Metro, and Charleston led the pack with solid year-over-year occupancy improvements, supported by steady in-migration and waning new supply.

Meanwhile, Midwestern markets including Kansas City, Columbus, and Detroit showed modest declines, a departure from peak pandemic-era levels. Overall, the data could indicate that stabilized occupancy is likely to persist into Q4 2025, even as developers scale back new starts.

Rent Growth Falls to Lowest Point Since 2015

Nationally, the SFR market saw a slight pullback in September, with advertised rents falling by $15 to $2,194, marking the weakest monthly performance in a decade.

Several markets posted notable rent gains in September, despite the sector’s overall slowdown. Twin Cities (+5.7%), Kansas City (+5.2%), and Chicago (+4.7%) stood out, outperforming the flat national trend – mainly due to consistent demand and limited new supply, which helped keep rents moving upward even as averages in other markets leveled off.

At the other end of the rent rates spectrum, declines were most pronounced in Tampa–St. Petersburg (-3.5%), Austin (-2.8%) and Denver (-2.4%). The pullback in these markets (much like in others, such as Jacksonville or Raleigh-Durham) aligns with recent deliveries and moderate leasing activity, which affected advertised rates in areas that had been growing quickly in recent years.

As the build-to-rent sector appears to be settling into a calmer phase, September numbers point to a steady market where most BTR SFR communities are maintaining high occupancy levels.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – August 2025

SFR BTR in August: Rents & Occupancy Rates Virtually Unchanged, “Accidental Landlords” Shake up Rental Market

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

August SFR Market Insights:

- Occupancy remained stable and high across the U.S. at 95%, with no month-over-month fluctuations, but year-over-year it has seen a 0.2% decrease.

- In August, average advertised rents for single-family BTR units remained almost unchanged at $2,208, but were up 0.6% compared to the same time last year.

- New Trend: Homeowners are increasingly opting to rent instead of sell, becoming unexpected rivals for institutional landlords.

A new trend is starting to gain an increasingly strong footing on the single-family rental market: The “accidental landlords,” or homeowners who choose to hold on to their properties and rent rather than sell amid high mortgage rates and weak demand, are inadvertently becoming competition for institutional landlords.

This is good news for renters, who might gain a bit more leverage when it comes to asking rates given that the total single-family rental inventory is seeing a slight bump, especially in the cities where these owners are joining the ranks of landlords in more significant numbers. And in some markets, that bump isn’t even slight. In Sun Belt markets such as Atlanta, Phoenix, Dallas, Houston and Tampa, where total rental inventory has jumped more than 20% in the past year, according to CNBC, renters can truly expect growing supply to affect local rents.

What’s more, rising costs and the softening job market are creating the conditions for rents to stagnate. Although the growing uncertainty about consumers’ financial health is not great news, it too contributes to the general month-over-month stagnation in asking rental rates.

In August, Occupancy Rates Held Steady at 95%, Nearly Unchanged Year-Over-Year

Sustained population growth kept demand steady, while the slowing supply growth and great absorption rates ensured occupancy levels remained high.

The national occupancy rate held steady at 95% in August compared to the previous month, posting no significant year-over-year changes either. Several markets, led by Sun Belt’s Miami, Jacksonville, San Antonio, Dallas-Ft. Worth, and Tampa have made occupancy gains due to ongoing strong absorption. Eleven more markets also posted gains.

This resilience is striking because it goes to show how severe the housing shortage in these areas really is and how much renters benefit from the expanding housing inventory, especially given that many of these markets are among the top 10 metros with the highest inventories of SFR BTR.

Single-Family Rental Rates Moved Very Little in August

Despite the rising competition coming from “accidental landlords,” the average rental rates held steady in August at $2,208, but they were slightly up year-over-year, posting a 0.6% uptick. That’s mostly due to the fact that demand remains high, as the market conditions in the for sale segment keep both sellers and buyers out.

While the Federal Reserve is expected to cut rates by at least 25 basis points in September, with gradual cuts likely to follow before the end of the year, their impact might not be enough to bring sellers and buyers back on the market in droves.

Zooming in on the changes at metro level, rents were up in 18 markets and down in 11, with only Atlanta rental rates not budging since July. While the Georgia capital is the only one to stay flat, asking rents in Houston; Miami Metro; Nashville; and Charleston were also virtually unchanged, with gains of less than 1%.

However, some things might change: With mortgage rates likely to remain quite elevated despite cuts, increasingly more homeowners may choose to stay put and hold onto their homes, putting pressure on institutional single-family BTR owners.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – July 2025

Steady SFR BTR Occupancy in July as Rents Ease Across Select Markets

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

July SFR Market Insights:

- Occupancy remains high across the U.S. at 95%, with Jacksonville (up 2.9%), Indianapolis, and Miami metro recording the strongest year-over-year gains.

- In July, advertised rents for single-family BTR units rose to an average of $2,205, up 0.4% from a year ago.

Demand for single-family build-to-rent homes (SFR BTR) remained strong in July 2025, as national occupancy rates held steady despite broader market pressures. As competition stiffens across the build-to-rent sector, amenities like swimming pools, jogging trails, pet parks, and on-site maintenance are making the difference in attracting and retaining tenants, particularly within larger developments.

Amenities are increasingly viewed as strategic tools that differentiate properties and bolster retention. And, for BTR SFR developers and managers, this means navigating a balancing act: maintaining high occupancy levels while optimizing rent levels in an ever-evolving environment defined by quality-of-life enhancements.

Occupancy Holds Steady Nationally & Rises in Select Metros, Including Up 3% in Jacksonville, FL

According to the July Yardi Matrix report, national occupancy for SFR properties stood at 95%. Though the national rate slipped 0.3% year-over-year, several markets posted significant gains.

Leading the occupancy growth rankings, Jacksonville, Indianapolis, and Miami metro showed gains between 1.8% and 2.9% year-over-year. In contrast, Columbus, Central Valley, and Harrisburg posted the most notable occupancy decreases, each down about 2% compared to the previous year.

The build-to-rent model within the single-family sector continues to demonstrate resilience; purpose-built SFR communities benefit from reasonable delivery timelines and increasing institutional investment. These factors, combined with persistent demand driven by household formation and relative affordability compared to homeownership, have contributed to stable occupancy and selective market-level growth.

Rent Performance Softens Across Half the Markets Analyzed

In July, advertised rents for single-family BTR units rose $3, reaching an average of $2,205, representing a 0.4% annual increase. This month, the top 30 SFR-BTR markets tracked are evenly split between those with positive and negative rent growth.

Among the top performers in year-over-year rent growth, Chicago led with increases close to 6%, followed by Harrisburg, PA, and Columbus, OH, up just under 5% each. These year-over-year gains in rent registered in these markets suggest stable and even growing demand for single-family rentals.

Granted, rent appreciation is being shaped by localized fundamentals such as employment growth, inventory levels, and migration patterns. The divergence in performance across metros reflects an increasingly segmented market landscape. So, while the national average rent increased slightly from the previous year, many metros saw rents decline, a reflection of localized shifts in supply, demand, and affordability strategies.

The most notable rent decreases were observed in South Dakota (down 4.2% year-over-year), Raleigh, NC (-3.4%), and Indianapolis, IN (-3.2%). Several others, such as Austin and Tampa, follow closely behind with annual rent drops of 2.9% and 2%, respectively.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – June 2025

SFR Performance Remains Solid in June, with Occupancy Rates Stable Month-over-Month

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

June SFR Market Insights:

- In June, national single-family rental rates rose 0.7% (which translates to a net of $4) year-over-year. This means the average rent crossed the $2,200 milestone, reaching $2,201.

- Metros that led in rent growth in June were Chicago (6.1%), Kansas City (up 5.5%) and the Inland Empire (4.5%). On the other hand, markets like Raleigh-Durham (-3.9% year-over-year), Austin (-2.9%), and Tampa-St. Petersburg (-2.5%) recorded the most significant decreases.

- U.S. SFR occupancy rates remain stable at 94.9%, despite a minor year-over-year drop of 0.5%.

The single-family rental market, and the rental market as a whole is navigating some choppy waters, with June bringing mixed news on the housing front. On the positive side, this month brought quite encouraging legislative developments aimed at addressing the ongoing housing crisis. In California, a new law was passed that should speed up housing development by cutting down on expensive, time-consuming environmental reviews. This reform is expected to help fast-track the construction of much-needed housing, signaling that state lawmakers are taking meaningful steps to increase supply.

At the same time, the economy and job market are doing well overall, but things are starting to slow down a bit. Unemployment is low, but fewer people are changing jobs, which can mean less movement and opportunity in the job market. On top of that, delays and uncertainty around new trade rules are making it harder for construction businesses to plan ahead.

According to Doug Ressler, “The future of the single-family rental (SFR) market and the broader U.S. rental market looks stable and growth-oriented, though nuanced by regional dynamics and economic pressures.“

SFR Occupancy Rates Almost Unchanged Month-over-Month, but Down Slightly Year-over-Year

According to the June Yardi Matrix report, the latest national occupancy rate for single-family rentals held steady at 94.9%. After the past few years have brought record deliveries, with a record number of units currently under construction, these stable occupancy rates point to resilient demand.

Many single-family rentals in 50+ communities all over the country have been absorbed through May, per Yardi Matrix, putting the market on track for another year of robust demand. While this is a slight dip compared to the previous year — and below the 97% peak seen in 2021 — the rate has remained relatively stable.

Tampa-St. Petersburg; Austin & Raleigh-Durham Post Biggest Rent Decreases

Last month, the top 30 SFR-BTR metros were almost evenly split between those with positive and negative rent growth. However, this month, advertised rates for single-family build-to-rent units increased in 17 markets, with only 12 recording (more modest) drops.

Nationally, average U.S. SFR advertised rents surpassed $2,200 for the first time in June, albeit by a small margin.

This goes to show that demand remains strong and the fundamentals behind the SFR BTR market remain solid, despite record-high deliveries and equally impressive numbers of units under development.

Looking at the most significant rent increases, it’s Chicago (6.1% year-over-year), Kansas City (up 5.5%) and the Inland Empire (4.5%) that snatched the top spots. This could be due to lower inventories in the area, which lead to an imbalance between supply and demand, creating a dynamic that favors rent growth.

On the other hand, there are markets where rents are decelerating, favoring renters. Metros posting negative SFR-BTR rent growth in June include Raleigh-Durham (-3.9%year-over-year), Austin (-2.9%), Tampa-St. Petersburg (-2.5%), and Cleveland-Akron and Indianapolis, both at -2.3%. Many of the markets with negative growth are impacted by rising total rental supply (including multifamily) and falling home prices, which provide more options for households.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – May 2025

Split Trends in May: Half of Top SFR-BTR Markets See Rent Gains, Others Face Downward Pressure

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

May SFR Market Insights:

- Nationally, single-family rental rates rose in May, reaching $2,183. However, year-over-year changes show a slight, 0.1% drop.

- Metros that led in rent growth in May were Detroit (5.0%), the Inland Empire (4.9%) and Kansas City (4.1%). On the other hand, markets like Austin (-4.4% year-over-year), Tampa (-3.3%), Phoenix (-2.5%) recorded decreases.

- U.S. SFR occupancy rates remain stable at 94.8%, despite recording minor year-over-year fluctuations.

The build-to-rent market might be entering a more measured phase. The sector remains resilient but the latest projections suggest that activity will taper off in the near future. Developers are now navigating rising construction costs, persistent labor shortages, and tighter financing conditions, all of which are expected to moderate the sector’s rapid expansion. Yardi Matrix forecasts a 44.5% drop in completions by 2027 compared to 2025, signaling a shift from explosive growth to a more sustainable trajectory.

Despite these headwinds, the fundamentals behind BTR remain solid. As affordability challenges continue to keep many households out of the for-sale market, and lifestyle shifts favor rental flexibility, investor interest in purpose-built rental communities is expected to remain high — especially in high-growth Sun Belt metros where population and job gains support long-term demand.

SFR Occupancy Rates Almost Unchanged Month-over-Month, Down 0.6% Year-over-Year

No matter the market, demand for single-family rentals remains consistent — and it’s expected to stay that way due to shifting demographics and evolving lifestyle preferences. According to the May Yardi Matrix report, the latest national occupancy rate for single-family rentals held steady at 94.8%. While this is a slight dip of 60 basis points from the previous year — and below the 97% peak seen in 2021 — the rate has remained relatively stable.

Although for sale prices are declining in several markets as well, giving potential home buyers some much needed motivation and hope, affordability remains vital when assessing housing options. Therefore, as long as the average monthly mortgage payments far outweigh the average monthly rent, many people and households will continue to rent, taking advantage of single-family rentals’ other perks as well: flexibility, fewer maintenance responsibilities, privacy, more space, and access to backyards.

Austin, Tampa & Phoenix Post Most Significant Rent Drops

According to Yardi Matrix, the top 30 SFR-BTR metros are almost evenly split between those with positive and negative rent growth.

Looking at the most significant rent increases, it’s Detroit (5.0% year-over-year), the Inland Empire (4.9%) and Kansas City (4.1%) that lead the way. This could be due to lower inventories in the area, which lead to an imbalance between supply and demand, creating a dynamic that favors rent growth.

On the other hand, there are markets where rents are decelerating, favoring renters. Metros posting negative SFR-BTR rent growth in May include Austin (-4.4%year-over-year), Tampa (-3.3%), Phoenix (-2.5%), Dallas (-2.1%) and Jacksonville (-0.1%). Those same markets are also among the leaders in declining home prices, per Redfin: Jacksonville (-3.4% year-over-year), Austin (-3.0%), Phoenix (-2.1%), Tampa (-1.3%) and Dallas (-0.8%). Many of the markets with negative growth are impacted by rising total rental supply (including multifamily) and falling home prices, which provide more options for households.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – April 2025

Sun Belt Markets Lead in Single-Family Build-to-Rent Inventory

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

April SFR Market Insights:

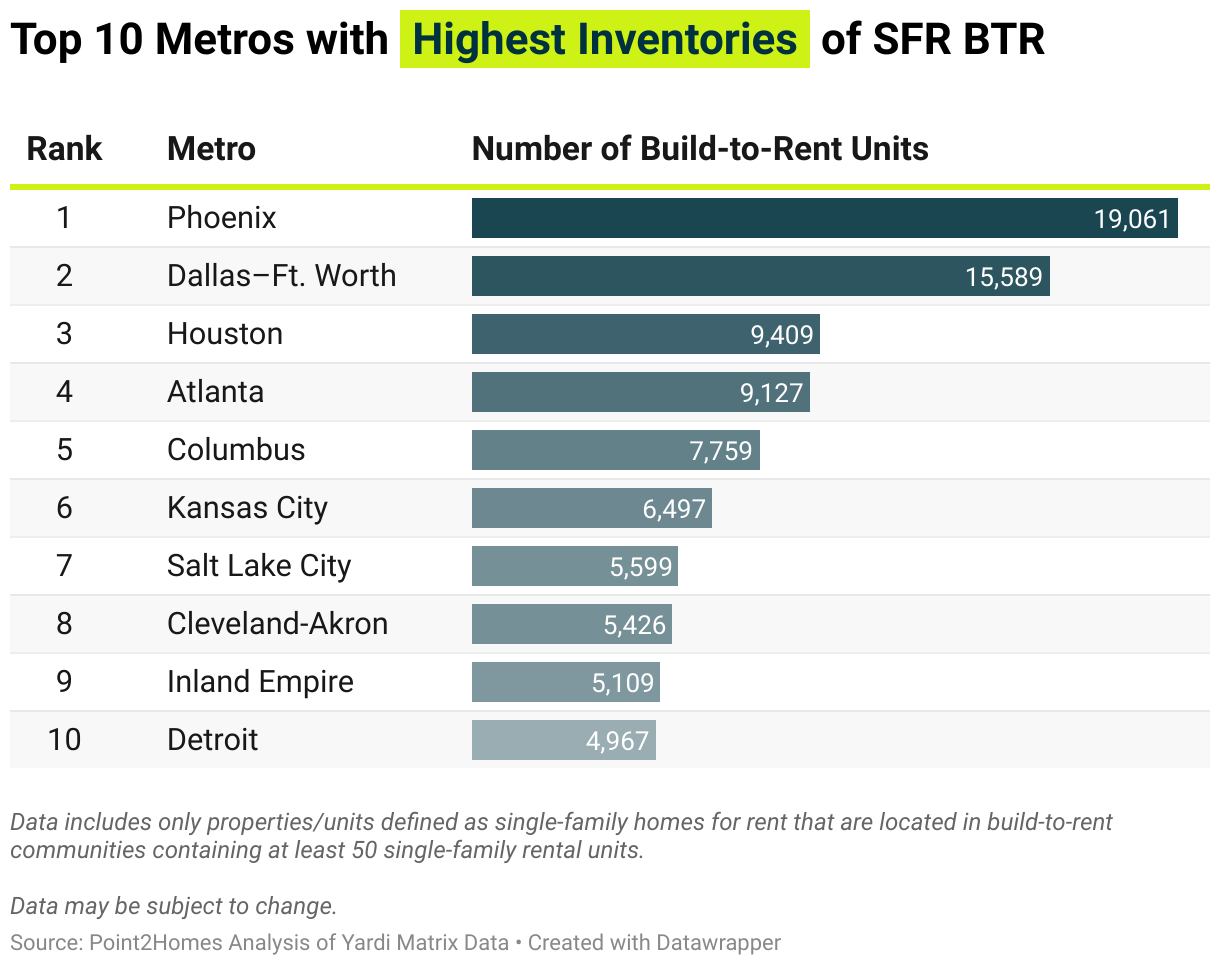

- In April, nine U.S. metros had 5,000 units or more in single-family build-to-rent communities with 50 or more units. BTR stock remains concentrated in high-growth Sun Belt metros such as Phoenix (19,061 SFR units), Dallas–Ft. Worth (15,589), Houston (9,409), and Atlanta (9,127).

- Rents dropped in half of the nation’s major markets in April, with Sun Belt cities like Austin (-4.4% y-o-y), Phoenix, and Dallas among the steepest declines.

While the build-to-rent market remains resilient, the latest projections suggest that activity will taper off in the near future. Rising construction costs and ongoing labor shortages are expected to slow the sector’s exponential growth, with the latest data from Yardi Matrix projecting a 44.5% drop in national completions by 2027 compared to 2025.

Even so, demand remains strong. As homeownership becomes increasingly unaffordable and renters continue to seek more space, developers are pressing ahead with new single-family rental communities. According to the April Yardi Matrix report, the BTR SFR market maintains strong momentum with a stock of nearly 230,300 single-family units nationwide.

Build-to-Rent Activity Strongest in Phoenix as Sun Belt SFR Supply Expands

The BTR sector continues to account for a significant share of new rental supply, with current single-family home developments expected to sustain steady delivery volumes through 2025.

As per Yardi Matrix, “The wave of supply will continue to suppress rent growth until the new units are absorbed, with a slowdown in completions anticipated in the coming years.” In 2025, Phoenix, AZ, alone is projected to add 7,144 new SFR units, which represents 1.9% of its total rental stock. Dallas, TX, is forecast to see 3,164 new units (0.3% of total stock), while Austin, TX, is expected to add 1,353 units (0.4%).

Nine out of the ten metros with the highest SFR BTR inventories are located in the Sun Belt, with Phoenix at the forefront, boasting over 19,000 built-to-rent houses. The area continues to be a hotspot for BTR investment, driven by strong in-migration, job growth, and sprawling land availability to sustain construction demand.

Rent in Half the Nation’s Major Markets Declined in April

According to Yardi Matrix, April advertised rent dropped in 15 out of 30 metros, while the year-over-year growth was flat at the national level. Single-family rental markets in the Sun Belt are facing the sharpest year-over-year rent declines, with nine of the ten metros seeing the lowest drops located in the region.

Austin, Phoenix, and Dallas stand out for both their significant projected supply growth in 2025, as well as declining rents. Rents in Austin have dropped 4.4% year-over-year, Phoenix has seen a 3.2% decline, and Dallas rents are down 2.1%. Together, these drops, plus the influx of new supply, are expected to moderate rent growth, potentially flattening rent trajectories in the near future.

As reported by Yardi Matrix, Detroit and Inland Empire are among the few markets to record a year-over-year increase in advertised rents for single-family rentals exceeding 5%. In both areas, strong demand has kept pressure on rents: In Detroit, growing interest in higher-quality rental housing and renewed economic activity have driven prices up, while in Inland Empire, spillover demand from Los Angeles continues to push rents higher.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – March 2025

SFR BTR Stock Remains Concentrated in Sun Belt Metros and the Inland Empire

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

March SFR Market Insights:

- In March, only eight metros had 5,000 units or more in single-family (SFR) build-to-rent (BTR) communities with 50 or more units. Geographically, build-to-rent inventory remains concentrated in high-growth Sun Belt metros such as Phoenix (17,438 units), Dallas–Ft. Worth (14,481), Houston (9,209), Atlanta (8,730), Columbus (7,600), Kansas City (6,299), Salt Lake City (5,450) and the Inland Empire (5,109).

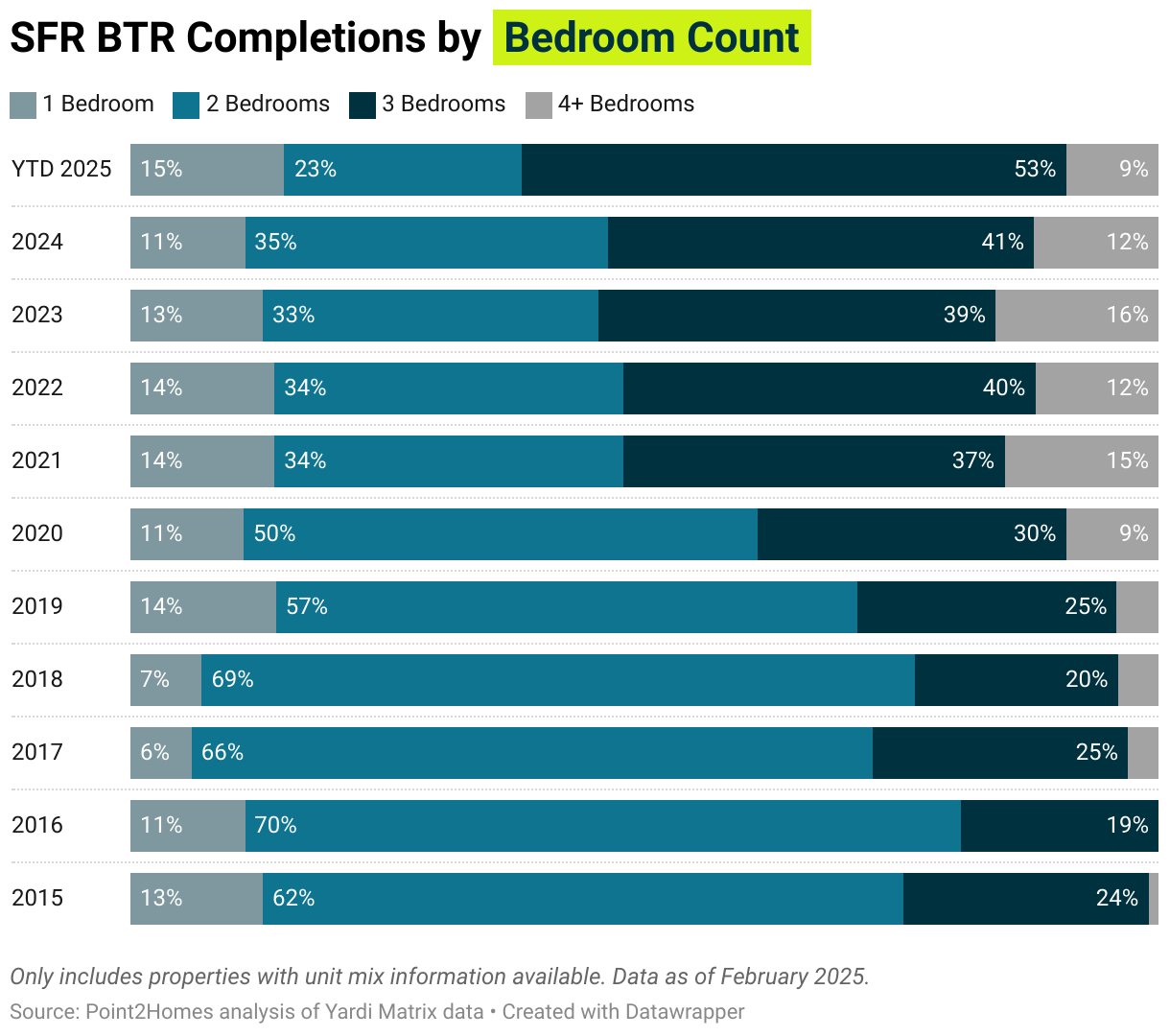

- Two-bedroom units no longer represent the majority of single-family build-to-rent completions, as three-bedroom house rentals continue to gain popularity.

- Occupancy rates for single-family rentals (SFR) remain high at 94.7%, showing no change from the previous month.

Rising construction costs and labor shortages are expected to dampen the exponential growth of the BTR sector. However, demand driving factors such as growing unaffordability and renters’ need for space continues to fuel the development of single-family rental communities. According to the latest Yardi Matrix SFR BTR report, the sector barrels along with nearly 110,000 single-family houses for rent across the country.

While the build-to-rent market remains resilient, projections indicate a moderate slowdown in construction activity post-2025. Single-family BTR project starts are forecasted to decline by 6%, and multifamily deliveries are expected to drop by 14%, according to industry data. Despite this, the BTR sector continues to represent a substantial portion of new rental supply, with current development pipelines positioned to maintain steady delivery volumes through 2025.

U.S. SFR Occupancy Rates Stable at 94.7%, Almost Unchanged Year-Over-Year

No matter the market, demand for single-family rentals remains strong — and it’s expected to stay that way due to shifting demographics and evolving lifestyle preferences. The latest national occupancy rate for single-family rentals held steady at 94.7%. While this is a slight dip of 70 basis points from the previous year — and below the 97% peak seen in 2021 — the rate has remained relatively stable, with very few chances of decline ahead.

Today’s SFR renters run the gamut from families with children and pets looking for a home with a yard, to divorcees who have children and/or want to retain the types of homes they lived in pre-divorce and from remote workers who need space for home offices to high-income millennials who are increasingly renters by choice, preferring BTR’s commitment and maintenance-free nature.

Affordability remains a key driver. With home prices high and the monthly cost of owning — including mortgage payments, taxes, insurance, and maintenance — far outpacing average rent, many households are choosing to rent, temporarily or by choice. Some renters are saving for a future down payment, while others are unable to qualify for a mortgage. Either way, they’re finding stability in the SFR market.

Three-Bedroom Overtake Two-Bedroom Rentals, Become House Renters’ Top Choice

For years, completions for three-bedroom rentals hovered around 20% to 25% of the total yearly deliveries. Increasingly more renters were opting for single-family rentals, but two-bedroom homes represented the majority of new house rentals hitting the market.

In 2021, however, three-bedroom houses for rent overtook all other types of homes and have held steady at around 40% ever since. This year is set to mark a new milestone for the BTR sector: Year-to-date figures place three-bedroom completions at 53% of all deliveries, which means they currently represent the majority of all new house rentals becoming available for renters.

What’s more, renters in SFR communities tend to stay longer than those in multifamily units, boosting retention and keeping occupancy rates high. Economic factors like high home prices and mortgage rates, which force renters to spend more time saving for a down payment on a home, but also lifestyle-related factors like high-income young professionals choosing to rent rather than buy are reinforcing the strength of the single-family rental market and ensuring its continued growth.

Sun-Belt Metros Lead with Highest SFR Inventories

According to Yardi Matrix, “The amount of SFR-BTR stock remains relatively small and is not distributed evenly across the country. Only eight metros had as many as 5,000 units in SFR-BTR communities with 50 or more units.“

However, supply is concentrated — and continues to expand — in the states and metros that are seeing the most significant population growth. Therefore, developers are planning and building new BTR communities precisely where demand is strongest. Per the latest U.S. Census data, “Texas, the second-most populous state, had the largest numeric increase in the country, adding nearly 563,000 people for a total population of 31,290,831 in 2024.” Eight other states recorded population gains of over 100,000 people, most of which are also leaders in the BTR sector.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – February 2025

Single-Family Rental Occupancy Holds Steady, Reaches 97.6% in Raleigh, NC

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

February SFR Market Insights:

- Nationwide occupancy rates for single-family rentals stayed strong at 94.7% in February, despite a slight 0.7% dip year-over-year.

- The national advertised average rent for single-family rentals held steady at $2,165, showing little change from February of last year.

- A record-breaking 39,000 build-to-rent single-family homes were completed last year, marking the highest number ever. And the BTR expansion continues, with 109,900 more homes in the pipeline.

The single-family build-to-rent market continues to show stability, even as overall housing construction slows. According to the latest report from Yardi Matrix, both SFR BTR and multifamily housing completions are expected to decline following record deliveries last year, but build-to-rent homes will drop at a smaller rate.

Back in 2019, homes built with the purpose of renting accounted for 2% of supply, but by 2025, that share is expected to reach 6.3% and climb around 7% in 2026. This consistent demand is driven by affordability challenges in homeownership, shifting lifestyle preferences, and high investor interest.

While the BTR market remains resilient, experts predict that the rapid pace of construction will slow after 2025. SFR BTR projects are projected to fall by 6%, while multifamily deliveries will decline by 14%. However, the build-to-rent sector continues to make up a large share of the rental market, with more than enough supply underway to support healthy delivery levels this year.

Record Number of Build-to-Rent Houses, Phoenix at the Helm

Despite high costs signaling a potential construction slowdown, the popularity of build-to-rent homes has led to record-high construction in recent years. In 2024, 39,000 units were completed — almost five times the number of houses for rent built in 2020. Notably, Texas’ ample land availability and relatively lower construction costs contributed to the completion of nearly 7,000 single-family homes built for renting.

There are currently 109,898 SFR units underway, with thousands of new BTR SFR in some of the nation’s major markets. The SFR BTR leaders are:

Phoenix, AZ

Phoenix is the nation’s top market for build-to-rent projects, leading both in recent deliveries and future construction. In 2024, the area added over 4,460 new rental houses — a 5-year high in which Phoenix has quadrupled its supply.

This rapid expansion is fueled by the region’s ability to build outward, strong population and economic growth, resulting in high demand for single-family rentals and rentals overall. For the next two years, the February report from Yardi Matrix projects that Phoenix will add more than 8,600 new BTR homes, further solidifying its position as the nation’s largest build-to-rent market.

Dallas, TX

Dallas is the second major player in SFR BTR development, and it has also set itself apart in both recent completions and upcoming projects. In the past five years, the metro has added over 10,400 single-family rental homes — 3,200 of which were delivered in 2024. By 2026, Dallas is set to reach a new milestone with over 6,400 new BTR homes expected to be completed, as per Yardi Matrix.

Atlanta, GA

Atlanta is a top market for build-to-rent single-family homes, ranking third nationwide in 2024. Last year alone, 3,035 new single-family rental homes were completed — a massive jump compared to just 116 BTR homes built in 2020.

BTR growth might slow down in some areas, but Atlanta doesn’t seem to be one of them. Over the next two years, an additional 5,135 single-family rental homes are expected to hit the market, further solidifying its status as a BTR hotspot.

Nationwide SFR Occupancy Remains Solid at 94.7% in February, Slight Dip Y-o-Y

The single-family rental market has seen remarkable growth in recent years, drawing heightened interest from both developers and investors. This surge highlights a growing opportunity for industry professionals as demand for more space and privacy continues to rise — trends amplified post-pandemic and expected to remain key drivers in the market for the foreseeable future.

In February, U.S. SFR occupancy rates saw a slight 0.7% dip year-over-year but remained stable at just under 95%. This stability is reflected across major markets, with occupancy rates ranging from 91.6% in Charleston to nearly 98% in Raleigh-Durham, showing only minor fluctuations across the country’s largest markets.

National SFR Rent Locked at $2,165, No Significant Change from February 2024

The average advertised asking rent for single-family rentals remained largely stable in February, increasing just 0.2% year over year at the national level. Rents declined in more than half of the country’s 30 largest markets, with Austin, TX, experiencing the sharpest drop — nearing a 5% decrease. It experienced an influx of new supply, and its rental market, which had been fueled by an influx of remote workers and tech sector growth, is now showing signs of leveling out.

Similarly, the Pensacola and Raleigh-Durham markets also experienced a notable rent drop nearing 4%. As seasonal trends shift, Pensacola’s peak demand for coastal properties is starting to ease, while in the Raleigh area, the cooling rental market could reflect a slowdown in tech industry growth coupled with an increase in housing supply.

While some of the country’s largest markets experienced relief, others faced upward pressure due to factors such as strong demand, limited supply, and local economic conditions.

Detroit and Kansas City saw rent growth amid relatively affordable housing markets attracting steady demand, while areas like the Inland Empire and Central Valley faced supply constraints that kept prices elevated. Meanwhile, Nashville’s continued population growth contributed to rising rental costs.

Even with signs of a construction slowdown, the build-to-rent sector continues to expand with a significant pipeline of single-family projects. And as developers continue to roll out new BTR communities, the ongoing supply will help maintain the market’s momentum.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. Yardi Matrix data on BTR deliveries, under construction and planned projects as of March 20th, 2025. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

BTR SFR Report – January 2025

Stable Occupancy for Single-Family Homes at the Start of 2025

The monthly Point2Homes Build-to-Rent Single-Family Homes Market Report is powered by Yardi Matrix data.

January SFR Market Insights:

- Nationally, the advertised rates for single-family rentals increased by $5 in January, reaching $2,157.

- In January, occupancy rates for single-family rentals (SFR) held steady at 94.7%, showing no change from the previous month.

The build-to-rent (BTR) market is thriving, with occupancy rates staying near 95% as rental demand continues to rise. According to the January report from Yardi Matrix, growing home prices and affordability challenges are expected to further fuel interest in single-family rentals throughout 2025. Despite hurdles like rising construction costs and labor shortages, the sector remains resilient, with 109,900 new single-family rental homes under construction nationwide.

With home sales at a 30-year low (just over 4 million, according to the National Association of Realtors), more people are opting to rent as a long-term solution. As a result, the single-family rental (SFR) sector is gaining momentum, attracting increased investor interest and reinforcing its role as a key player in the housing market.

Single-Family Home Occupancy at 94.7% Nationwide, Soars Above 98% in Central Valley, CA

High occupancy rates in the BTR SFR sector show strong demand, even as the industry faces challenges like high material and labor costs, rising construction expenses, and concerns about oversupply — especially in areas with heavy development.

In January 2025, nationwide SFR occupancy rates saw a slight 0.7% dip year-over-year but remained stable at just under 95%, reinforcing the sector’s long-term potential. This trend is reflected across 30 of the country’s major markets, all displaying occupancy rates higher than 90%.

Hot markets like Central Valley, CA (98.3% occupancy); Raleigh-Durham, NC (97.5%); Inland Empire, CA (96.4%); Las Vegas, NV (96.2%), and Nashville, TN (96.1% after a 1.6% year-over-year increase) are seeing high demand for single-family rentals — a demand that remains strong as many are priced out of homeownership.

2025 Begins with $5 Boost in Advertised Rent for Single-Family Rentals

According to Yardi Matrix, advertised rent growth for single-family homes declined in Q4 of last year, as rent growth for build-to-rent single-family rentals generally lagged behind the multifamily sector — though results varied by location. In January, advertised rates for single-family rentals climbed $5 since December, bringing the national average to $2,157.

Advertised rents for single-family homes are falling in high-supply markets like Phoenix, Dallas-Fort Worth, and Austin. House rents in Austin actually experienced the steepest year-over-year rent decrease, dropping nearly 5%.

Against the backdrop of significant growth in both BTR SFR and multifamily development, renters in these markets may gain more bargaining power. At the same time, rising homeownership costs and high interest rates in such booming markets have kept many renters in apartments, reducing the demand for single-family homes and contributing to a slower rent growth.

In contrast, the smaller supply of houses built with the purpose of renting in markets like Kansas City and Detroit has helped sustain demand, leading to rent increases of 5.4% and 4%, respectively.

According to Yardi Matrix, SFR rent outperformed multifamily rent in some secondary metros — such as Greenville, SC, Salt Lake City, UT, and Denver, CO — where multifamily construction has driven down rents.

As we move into 2025, the built-to-rent single-family rental sector looks well-positioned to continue its growth, with steady occupancy rates and strong demand driven by ongoing homebuying challenges, rising construction costs, and concerns about oversupply in some markets.

Methodology

Point2Homes.com is a real estate listing portal for rental homes across the United States. Part of Yardi Systems, Point2Homes covers housing trends and news through comprehensive studies that draw from internal data, public records, governmental sources, and online research.

This report is based on data provided by our sister company, Yardi Matrix. The data includes single-family build-to-rent communities of 50 homes and larger. A Yardi Matrix market generally corresponds to a Standard Metropolitan Statistical Area (SMSA), as defined by the United States Bureau of Statistics.

Images: Allison H. Smith, Trong Nguyen / Shutterstock.com

Fair Use and Redistribution

We encourage and freely grant permission to reuse, host or repost these reports. When referencing the data, please credit and link Point2Homes, Yardi Matrix, or this page.

Kindly use phrases like “according to Point2Homes and Yardi Matrix” or “Data provided by Yardi Matrix via Point2Homes” to point readers to the monthly releases, the research and methodology behind them.

If you have any questions about using the data or want to get in touch with one of our analysts, feel free to contact us at [email protected].