Paying rent on time when renting a house isn’t just a routine task — it’s the key to maintaining financial stability and a good relationship with your landlord. If they miss a payment, renters could face serious consequences, from a damaged credit score to eviction in extreme cases.

While having a solid budget helps, it’s not always enough. A well-structured rent payment schedule tailored to your financial situation ensures you stay on track month after month. Rather than leaving things to chance, smart renters take proactive steps — including negotiating with landlords when needed — to guarantee their rent is paid on time, every time.

Different Methods for Paying Rent

The way renters pay their rent can significantly impact their ability to make timely, full payments. To stay on track, it’s important to explore the most common payment methods and weigh their pros and cons.

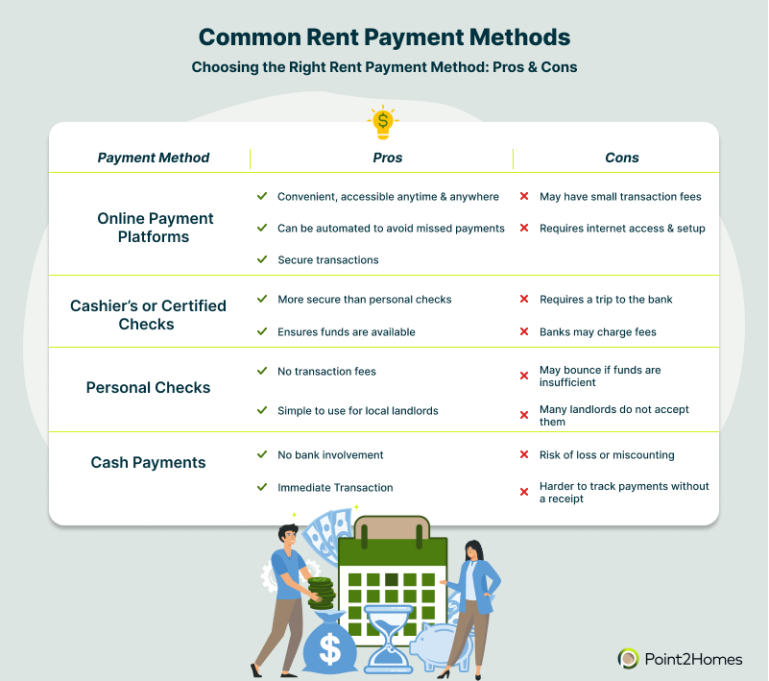

1. Online Payment Platforms

Many landlords and property managers now accept rent payments through online platforms or apps. These allow renters to pay anytime, from anywhere — perfect for those who travel or have a landlord who lives out of town. Renters should also choose a secure, reputable platform that protects their personal and financial information.

Some landlords require specific apps, while others let renters choose their own payment platform. Many of these services also offer automatic payments, ensuring rent is never missed as long as there are enough funds in the account.

Note: While convenient, online platforms may charge small fees, especially for card payments.

2. Checks: Cashier’s, Certified, & Personal

Yes, checks are still a common offline rent payment method, with cashier’s checks being the most secure option. These checks guarantee that funds are available, put a hold on the amount, and release it only to the recipient — giving landlords confidence that the payment won’t bounce.

Certified checks are another option, but they only confirm that funds were available at the time of writing, making them slightly less reliable. On the other hand, personal checks are rarely accepted due to the risk of insufficient funds.

Note: Paying with cashier’s or certified checks requires a trip to the bank, which can be inconvenient. Additionally, some banks charge fees for issuing these checks.

3. Cash Payments

Although some landlords still accept cash, it’s becoming less common due to the risks involved. Unlike digital transactions or checks, cash payments offer little security—money can be easily lost, miscounted, or even disputed.

One major drawback is the lack of a clear record linking the payment to the renter. While other payment methods provide a receipt or digital trail, cash does not automatically verify who made the payment. This can lead to confusion, especially for landlords managing multiple tenants. To avoid issues, renters should always have the landlord count the money in their presence and provide a written receipt.

Note: Cash payments must also be made in person, making them far less convenient than online transfers or mailed checks.

How To Ensure the Payment Schedule Works for You

Making sure the rent is paid on time is a priority for landlords and renters alike. As such, it’s important to strike the right balance and find a payment schedule that works for both parties. Here are a few tips:

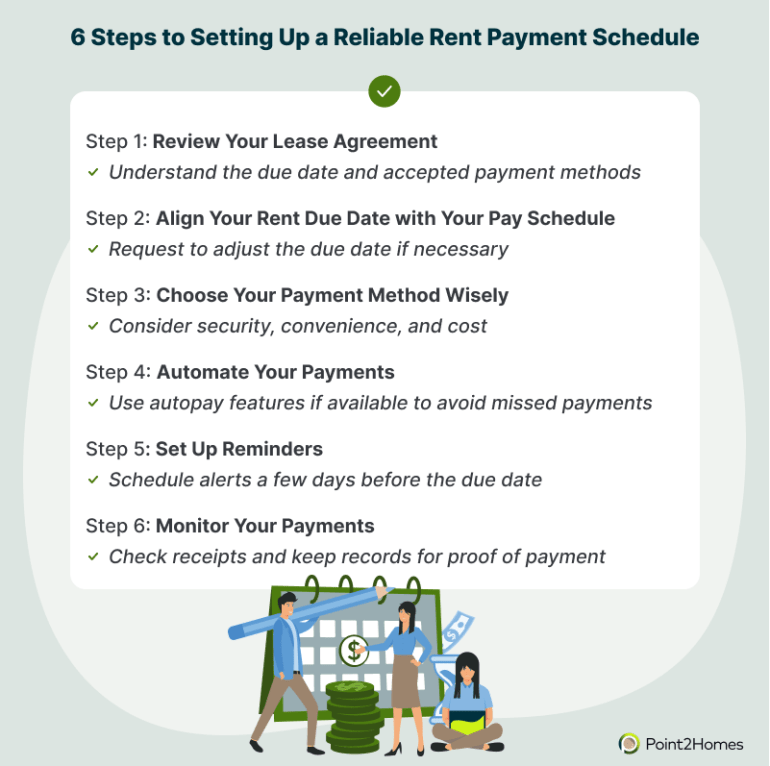

1. Choose a Payment Method That Works for Both Parties

With several rent payment options available, renters and landlords must agree on a method that works for both. Some landlords have strict preferences — especially those who use online payment platforms — while others may be open to different options.

Before signing the lease, renters should review the payment terms carefully to ensure they align with their financial situation and convenience. If needed, they can discuss alternative methods with the landlord to find a solution that ensures timely payments while meeting both parties’ needs.

2. Negotiate the Rent Due Date

Since most people get paid at the end of the month, rent is typically due shortly after. However, this isn’t always the case, so it’s important to check the lease agreement and ensure the due date aligns with when funds will be available. Ideally, renters should allow a buffer of a few days between payday and rent payment to account for any potential delays.

Many landlords are open to adjusting the due date if it ensures timely and complete payments. If a change isn’t possible, renters can consider paying early or transferring the rent amount to a separate account until the due date to avoid last-minute issues.

Find out more about handling late rent payments and what to do if you miss a due date.

3. Have Rent Payments Reported to the Credit Bureau

As an extra incentive to ensure the rent gets paid on time, renters may request that the landlord report the rent payments to the credit bureau. In addition, this enables renters to build their credit score. Unlike mortgage payments, rent payments don’t automatically appear on a credit report, but renters can request that their landlord or property manager report them.

4. Automate Payments

Setting up automatic payments is one of the most effective ways to ensure rent is paid on time, every time, eliminating the risk of forgetting to make a payment due to a busy schedule, travel, or unforeseen circumstances.

With this feature, rent is deducted automatically from the renter’s bank account or credit card on the scheduled due date, providing peace of mind and helping to maintain a strong financial reputation. Many online payment platforms enable automated payments with just a few clicks, making it much more convenient for renters.

5. Set up Reminders

Whether payments are automated or manual, setting up rent reminders a few days before the due date can be incredibly helpful in avoiding late payments. Renters can use online tools and apps or even request reminders from their landlord. These reminders serve as a proactive measure, giving renters enough time to ensure funds are available in their accounts before the rent is due and allowing them to take any necessary action to avoid delays. Additionally, setting reminders can help renters stay organized and ensure their finances are always in check, reducing the stress of last-minute payments.

Image credits: Alwie99d/stock.adobe.com; Dorde Krstic/Shutterstock.com