House, but Saving for Down Payment Takes Up to 94 Years")

How long does it take to save for a down payment on a home? More than the average life expectancy if you’re a Gen Z buyer in Irvine, Calif., but just around two years if you’re a higher-earning Gen X buyer in some large Midwest cities. Analyzing income and home price data for the 100 most populous U.S. cities, saving for the standard 20% down payment for a median-priced home would take between two and 94 years — depending on whether you’re a Baby Boomer, Gen X, Millennial or Gen Z homebuyer.

Being able to save enough for the down payment is the first hurdle on the path to homeownership. But, up until the spring of 2020, the national average savings rate had hovered around a meager 8%. Then, the pandemic completely changed Americans’ saving habits. For instance, in the past year, the national average savings rate ballooned to 17% — which means that people have been setting aside much more.

However, with home prices posting even stronger increases, buying a home might feel like chasing a moving target.

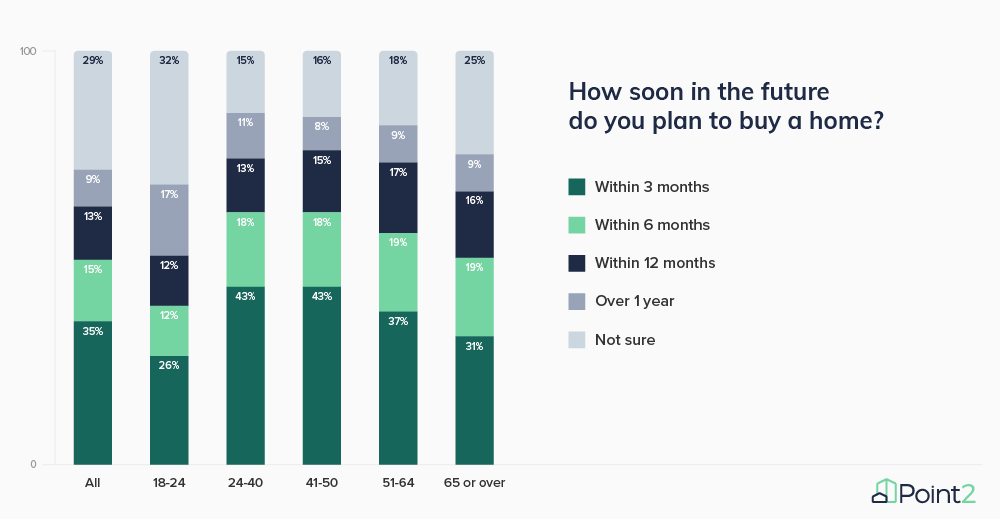

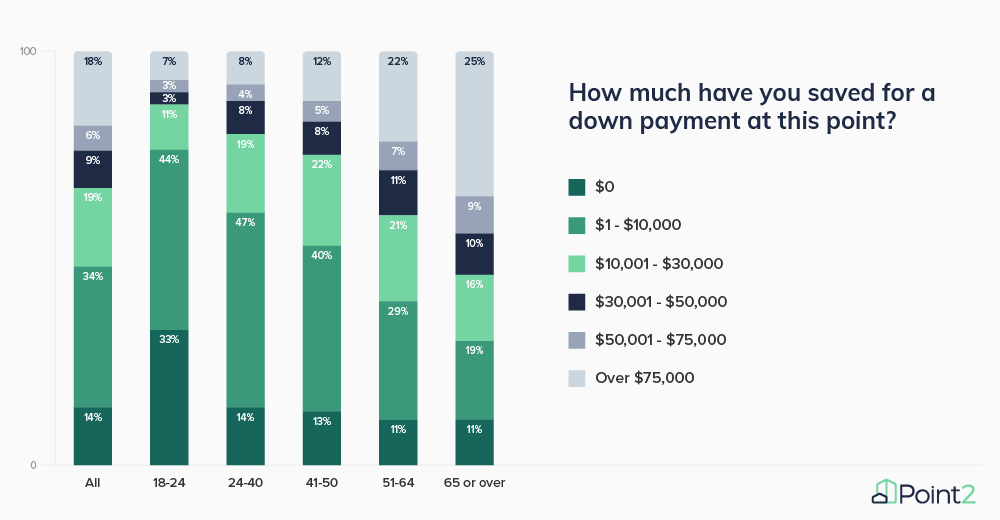

That’s because the national median home sales price reached $346,800 in the last quarter, bringing the down payment to almost $70,000. But, unfortunately, in a nationwide poll of nearly 7,000 prospective homebuyers surveyed on its listings platform last autumn, Point2Homes found that around 75% of home-seekers had much less than the average down payment, and 14% had no savings set aside yet. Responses also revealed that 50% of those who were looking for a home would like to buy one in the next six months and an impressive 70% of all respondents wanted to buy a house rather than a condo.

[metaslider id=”141421″]

- In the past year, the national average savings rate increased from 8% to an impressive 17%.

- Home prices recorded accelerated growth, and the standard down payment on a home followed suit, almost cancelling homebuyers’ saving efforts.

- The national median home sale price is almost $350,000, which means the standard 20% down payment is close to $70,000.

- At the current savings rate, Gen Z buyers would need more than 10 years to save enough for a down payment in 36 cities.

- On the bright side, Millennials, Baby Boomers and Gen X buyers would need more than 10 years of saving in only four cities. So, 96 urban centers are slightly more affordable markets for the older generations.

- A Point2Homes survey done in autumn last year revealed that 50% of home-seekers would like to buy in the next six months. But, 30% of all respondents expected to need less than $10,000 for a down payment and almost half of survey-takers had less than that in savings.

From Less Than 2 Years to Nearly 94, Buyers from Different Generations & Cities Are Looking at Wildly Different Timelines

Gen Z — a generation on the cusp of adulthood and the newest to enter the work force — has the lowest incomes and that’s why they’re also looking at the longest period of time needed to save for a down payment. For example, it could take between 23.5 and 20.9 years to save enough for a down payment in expensive cities like Los Angeles and San Jose, Calif., whereas it could be less than five years in cities such as Fort Wayne, Ind.; Buffalo, N.Y.; Garland, Texas; Cleveland, Ohio; and Detroit. Clearly, in some cities, Gen Z buyers might need to save for a very long time if they don’t have help.

In particular, one city that really stands out is Irvine, Calif. Here, with a high number of young people still in school and a low median income for this age group, it would take more than the average lifetime to save enough for a down payment.

Meanwhile, Millennials would need more than 10 years to save for a down payment in four California cities (Los Angeles; Long Beach; Oakland and Santa Ana), while Gen X and younger Baby Boomers might have affordability problems in four cities as well — just slightly different ones: San Francisco; Los Angeles; New York and Oakland, Calif.

And, much like their younger counterparts, older Baby Boomers (those in the 65+ age group) are looking at no fewer than 24 cities where it would take more than 10 — and even more than 20 — years to save for the recommended 20% down payment.

Check out the full table and switch between the tabs below it for more data on all the generations. Use the filters to reorder all 100 cities based on income, home price, or years needed to save for a down payment for each age group.

Millennial & Gen X Buyers Most Determined to Buy a Home in the Next 6 Months…

Two age groups — corresponding largely to Millennials and Gen X ers — had an almost identical profile when it came to their readiness (or lack thereof) to buy. Of these, a total of 61% were looking at a six-month buying timeline, while around 15% were just keeping an eye on the market and unsure when they might join the ranks of homeowners or change their current address.

Likewise, although 32% of Gen Z respondents were still pondering their options and considering a longer buying time frame, a not at all negligible 38% of young respondents stated that they wanted to buy within the next six months. And these young potential homebuyers have a reputation of being more budget-conscious and more deliberate when it comes to financial decisions. Therefore, buying a home might be a very appealing financial investment for them.

but Almost Half of Respondents Have Less Than $10,000 in Savings…

Despite the increase in the average savings rate, many Americans might not be directing the money toward their down payments. In fact, the pandemic and the financial instability that ensued has forced many people to reconsider their homebuying budgets — or to table their dreams for the time being. Furthermore, while some Americans kept their jobs and were financially secure enough to take advantage of the low mortgage rates and invest in a home, many others definitely couldn’t afford to maintain their previous buying plans.

To that end, survey responses also reflected the new reality: While we may be saving more, it’s not necessarily for a home. For instance, although 34% of respondents had up to $10,000 set aside for a down payment, 14% of this group had no savings yet. Unsurprisingly, Gen Z home-seekers were the least prepared, despite their desire to own: 33% of young prospective buyers didn’t actually have any money set aside. Millennials and Gen X followed at a distance, with a fair share of buyers from these age groups reporting that they had no savings for a down payment.

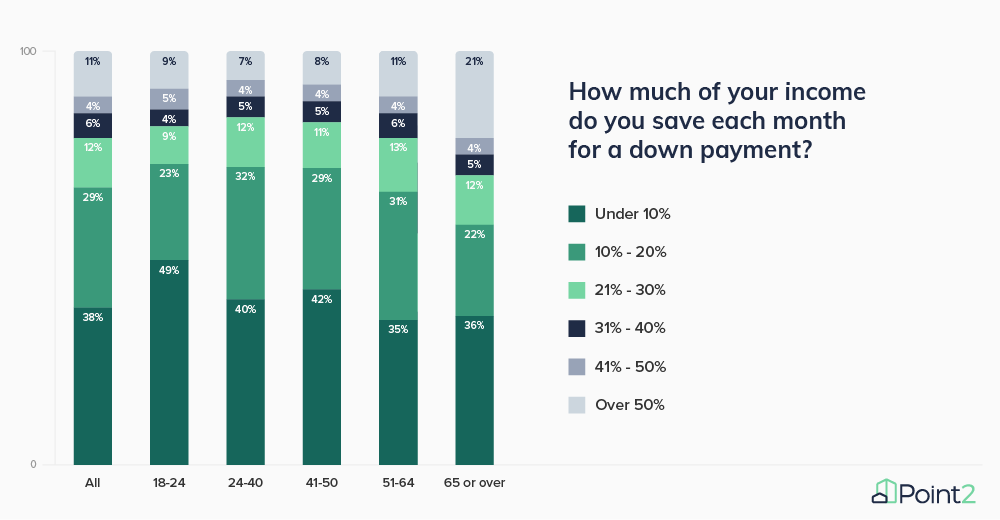

and Save Less Than 10% of Their Monthly Income

A lack of spending opportunities may have contributed to the increased savings rate, but the share of income that actually goes toward the down payment on a home remains small.

However, although the majority of prospective homebuyers directed less than 10% of their monthly income toward a down payment for a home, it’s worth noting that around 10% of house-hunters in each age group (and 21% of those older than 65) were setting aside at least half of their monthly income to cover down payment expenses — which makes them the most determined and also the most intentional buyers.

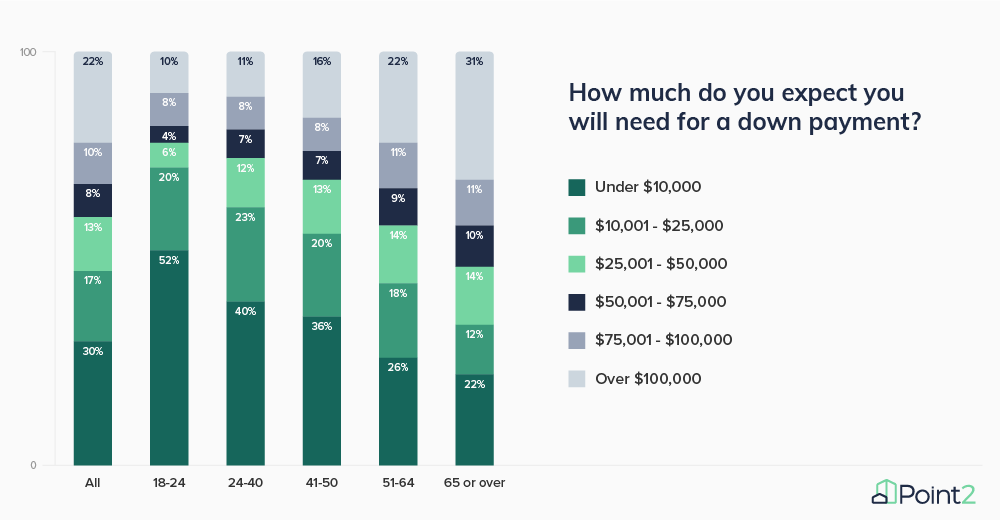

30% of Home-Seekers Expect to Need Less Than $10,000 for Down Payment…

Unlike rent, which is on a downward trend — especially in large coastal cities — home prices have reached new highs:

Home prices nationally increased 10.4% compared with December 2019, according to the S&P CoreLogic Case-Shiller Home Price Indices. That is the strongest annual growth rate in over six years, and a significantly stronger gain than in November, when prices were up 9.5%. It also ranks as one of the largest annual gains in the more than 30-year history of the index.

Accordingly, as home prices increased, the standard down payment for the median home also went up. But that is not what most home seekers are expecting. So, given that the average home is now close to $350,000, the 20% down payment is perilously close to a staggering $70,000. Nonetheless, 30% of respondents believed they would need less than $10,000, making it abundantly clear that their expectations might be sabotaging the homebuying efforts.

In fact, most Gen Z and Millennial respondents expected to need less than $10,000 to cover the down payment on a home. But, while first-time home buyers may be right to assume that starter homes will have lower prices, market conditions could work against them. That’s because many sellers are postponing putting their home on the market, and even new construction might be affected by low supply and growing prices. What’s more, according to CNBC, “A sharp drop in new listings partly due to severe weather, combined with already record-low supply, will make it increasingly difficult for buyers to find their dream home at the perfect price.”

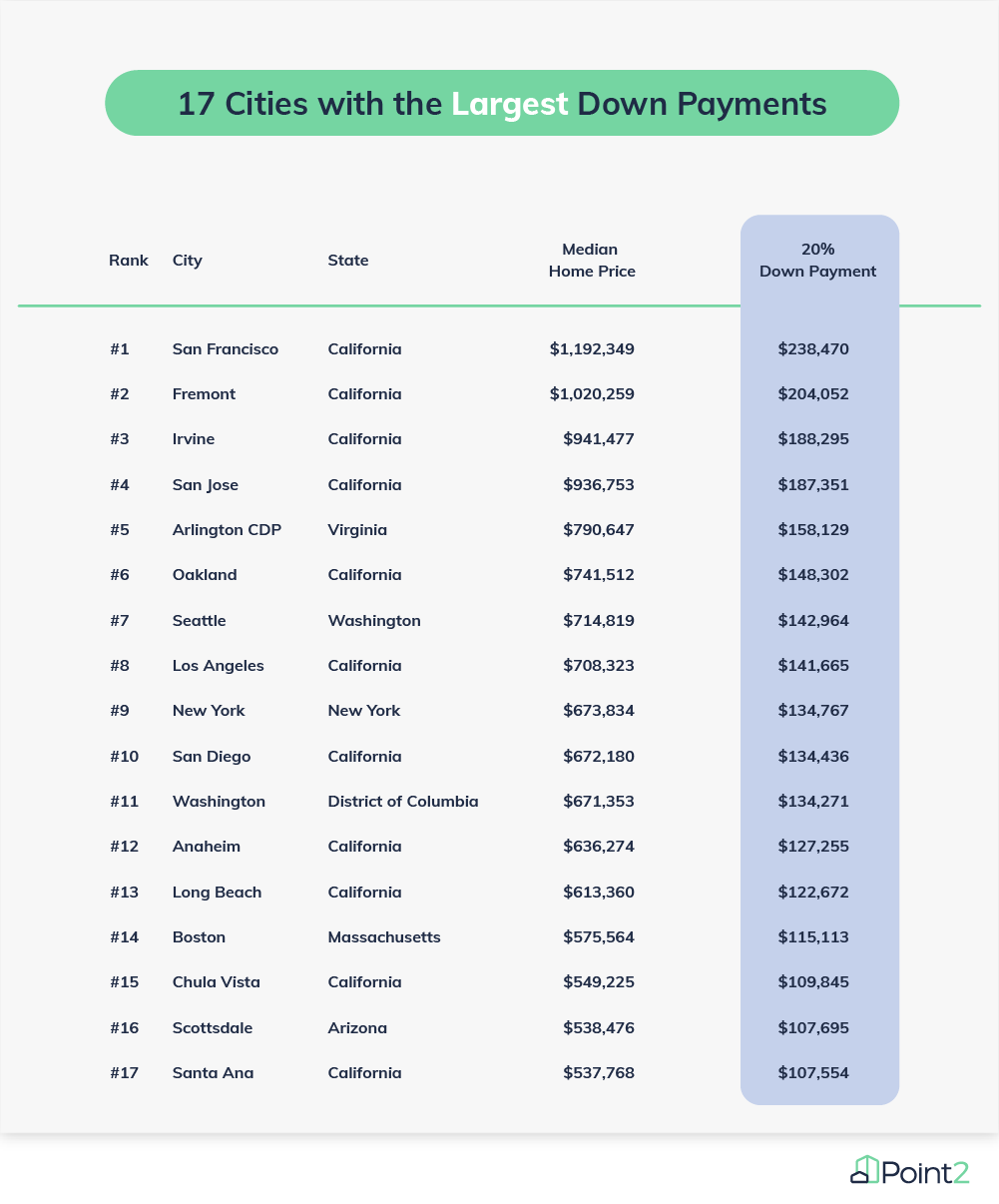

but in 17 Large U.S. Cities, Down Payments Are $100,000-$200,000

With median home prices that have crossed the million-dollar mark, San Francisco and Fremont, Calif. also have woefully unaffordable standard down payment amounts. To put that in perspective, the down payment alone in San Francisco is higher than the median home price in 44 other large U.S. cities.

This means that, despite the large differences in median income between Gen Z, Millennials and Baby Boomers, saving for the down payment in these cities might take a really long time for anyone interested in finding their forever home in these areas — no matter which age group they belong to.

Conversely, there are large cities where homes are more affordable, making it easier for buyers to save for a down payment in less time. For example, Detroit is the only city where the down payment amount actually coincides with the majority of buyers’ expectations. Here, the standard down payment for the median home is $10,796. Three more cities also have down payments less than $20,000: Buffalo, N.Y.; Toledo, Ohio; and Cleveland.

Most Home-Seekers Looking for Larger Houses May Be Wishful Thinking in Current Market

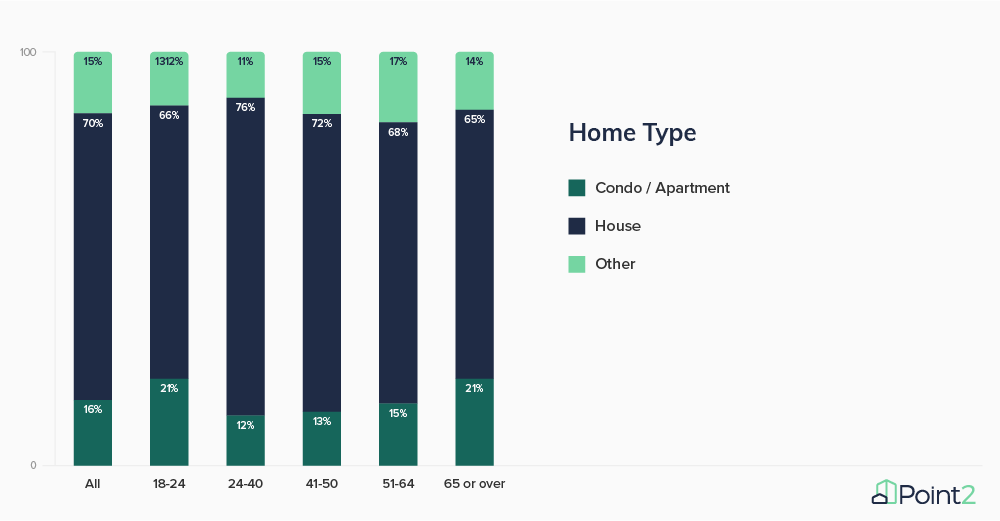

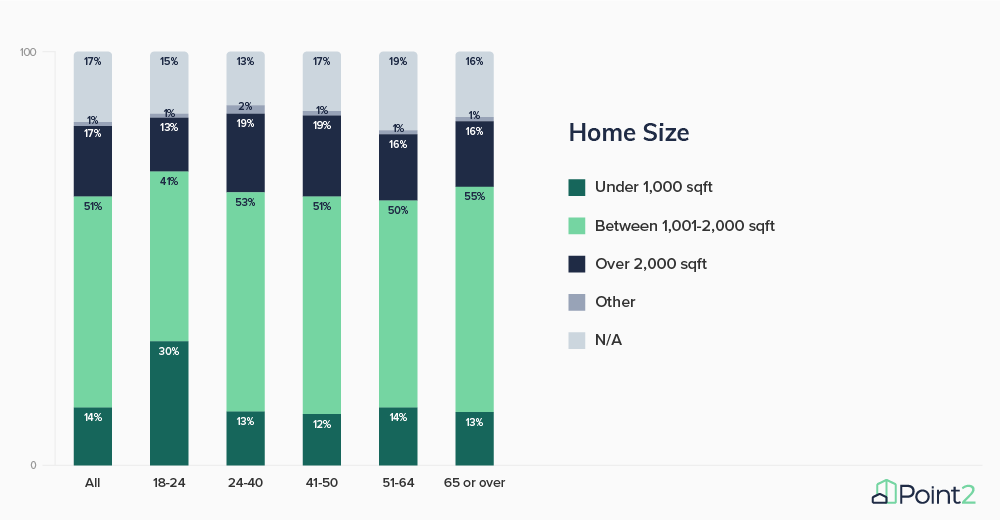

The pandemic accelerated many trends that were already underway, and the desire to buy a larger home was one of them. One of the most significant consequences of working from home was the need for more living space — and the answers to our survey reflect just that: 70% of respondents would prefer a house to a condo. Moreover, the majority (51%) were interested in houses between 1,000 and 2,000 square feet.

But a larger home might not be in the cards — and, this time, it’s not just the price that’s to blame. According to CNBC, large and small homes are in very short supply:

There were nearly half as many homes for sale at the end of February, compared with a year earlier. Low supply was exacerbated by a drop in the number of new listings to come on the market. A pullback by sellers resulted in roughly 207,000 fewer homes newly listed for sale in the first two months of 2021 compared with the average for the same period over the last four years.

Methodology

- This study was based on the 100 most populous cities in the U.S., sourced from the U.S. Census Bureau (2018). Population by age, American Community Survey one-year estimates.

- The median income per household, adjusted for inflation in January 2021, was sourced from the U.S. Census Bureau (2019). Median income in the past 12 months, American Community Survey one-year estimates.

- The median home price per city was sourced from the U.S. Census Bureau (2018). Median value (dollars), American Community Survey five-year estimates. The current, adjusted median home price was calculated based on the NAR index for Q3 of 2020 and the FHFA House Price Index for the months October, November and December 2020, as well as January 2021.

- The 20% down payment amount was calculated based on the median home price in each city.

- The number of years that prospective homebuyers would need to save for a down payment was based on current, adjusted median household income, adjusted median home prices, and average monthly savings rates sourced from Trading Economics.

- The survey was posted on the real estate platform Point2Homes.com between August 21 and September 7, 2020; 6,780 people participated.

Fair use and redistribution

We encourage you and freely grant you permission to reuse, host, or repost the story in this article. When doing so, we only ask that you kindly attribute the authors by linking to Point2Homes.com or this page, so that your readers can learn more about this project, the research behind it and its methodology.

Check out more interesting articles:

Best Cities for Millennials: Canada’s New Millennial Hot Spots [85 Cities Ranked]

[Moving to Boston] Just How Much Is the Cost of Living in Boston?

[Moving to Atlanta] Just How Much Is the Cost of Living in Atlanta?

For an overview of the real estate market in some of the areas mentioned in this study, visit the links below:

[columns size=”1/2″ last=”false”]

Washington Real Estate

Boston Real Estate

San Diego Real Estate

Seattle Real Estate

New Orleans Real Estate

Riverside Real Estate

Portland Real Estate

Anaheim Real Estate

Sacramento Real Estate

Richmond Real Estate

[/columns]

Newark Real Estate

Austin Real Estate

Chula Vista Real Estate

Arlington Real Estate

Miami Real Estate

Madison Real Estate

Baton Rouge Real Estate

Scottsdale Real Estate

Atlanta Real Estate

Denver Real Estate