Despite mortgage rates reaching historic lows, housing affordability continues to erode in the country’s largest and most in-demand cities. In a year as volatile and uncertain as 2020, the effect of lower mortgage rates was muted by soaring home prices, increasing demand and tight supply.

In fact, the share of income needed to afford housing continues to increase and monthly mortgage payments are becoming a financial burden in more cities across the nation. For example, in 2010, homeowners in 13 large cities paid more than 30% of their income to cover the mortgage. Now, in 2020, new homeowners in no fewer than 15 cities are financially burdened by their recently acquired mortgages.

Our latest study shows that the increase in income is no match for the rapidly increasing home prices in the 100 largest U.S. housing markets. And this disparity between galloping home prices and slower-moving incomes means that mortgages take up incrementally more of homeowners’ hard earned money each year. It also means that the number of unaffordable cities, where homeowners spend more than 30% of their income to cover the mortgage alone is going up as well.

Here are the mortgage affordability study highlights:

- Mortgage affordability worsened in 51 of the 100 largest U.S. cities. In 11 cities the share of income spent on mortgage remained relatively unchanged.

- In the last decade, the median home price crossed the $1 million mark in three cities, all of them in California: San Francisco, Fremont and San Jose.

- Home prices are increasing faster than wages in 53 of the nation’s 100 largest cities.

- The number of cities where mortgages alone take up more than 30% of homeowners’ income is 15 in 2020, up from 13 in 2010. The majority of cost-burdened cities are on the West Coast.

- Homebuyers in the most unaffordable cities would need to earn up to $43,567 more to avoid being cost-burdened.

- Newark, NJ is the only market to exit the unaffordability list: the city’s mortgage unaffordability rate decreased from 34% in 2010 to 27% 10 years later. Meanwhile, California cities Santa Ana, San Jose and Fremont experienced just the opposite: they were not on the list 10 years ago, but the average mortgage in these locations now represents more than 30% of income.

- The six large cities where mortgages account for the least amount of homeowners’ income (10% and under) are Memphis, TN, Laredo, TX, Fort Wayne, IN, Toledo, OH, Cleveland, OH and Detroit, MI.

The Least Affordable Cities: Number of Unaffordable Markets Goes From 13 in 2010 to 15 in 2020

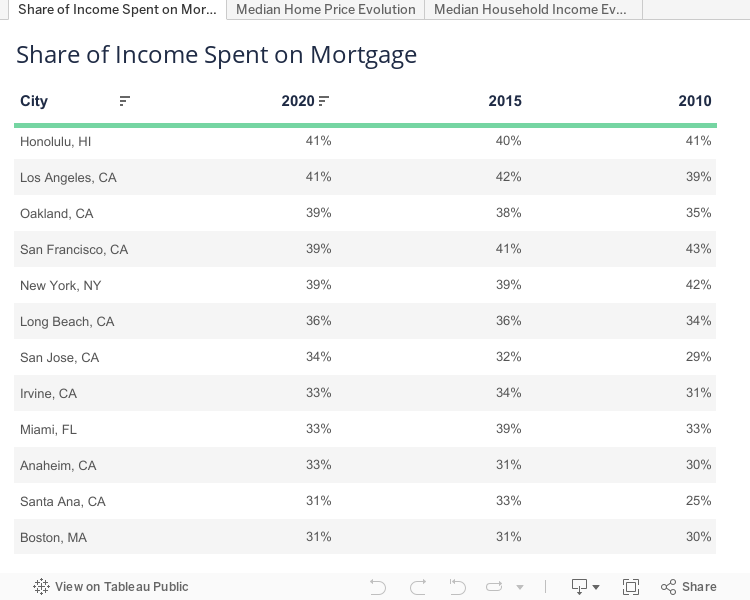

Compared to 2010 — when San Francisco and New York City homeowners dished out 43% and 42%, respectively, of the median income to cover the mortgage — in 2020, owners in both cities are looking at a slightly improved situation: the mortgage currently eats up a little less (39%) of the median income in these cities.

Newark, NJ, is the only city to leave the list of unaffordable markets. While 2010 mortgages took up 34% of residents’ income, 2020 mortgages — representing only 27% of the median income — are a definite improvement.

The three markets that did not make the most unaffordable cities list in 2010 are Santa Ana, San Jose and Fremont, all in California. In 2020, however, they crossed the 30% mark, joining veteran unaffordable markets like San Francisco, New York City and Honolulu, HI.

In fact, Hawaii’s capital and largest city was the third-most unaffordable large U.S. city in 2010, but it reached the top position on this infamous list this year. Moreover, although the majority of the cities in the list have seen some fluctuations, Honolulu is the only city where mortgages have taken up more than 40% of homeowners’ incomes in 2010, as well as in 2015 and 2020.

In 5 Cities, More Than 50% Difference Between Increases in Home Prices & Incomes

Since 2010, home prices in Los Angeles have increased 57%. But that seems almost reasonable compared to cities like Seattle and Santa Ana, where prices went up 77%, Fremont, CA, which saw an 88% increase in just a decade or Oakland, CA, Aurora, CO and North Las Vegas, NV, where price tags are currently 90% and even 100% higher than 10 years ago.

However, there are no cities where the median income doubled in the past decade or cities where it increased 90%. In fact, the most impressive pay raises in the nation’s 100 largest cities were recorded in the country’s most famous tech and business hubs — Seattle and San Francisco. Here, incomes jumped 78% and 80%, respectively, in the last 10 years as companies such as Amazon, Microsoft and others expanded into Seattle office space rapidly. As an article in The Atlantic emphasizes:

The housing cost crises in the Bay Area and New York might be the country’s most obscene. But the problem is national, driven by a combination of stagnant wages, restrictive building codes, and underinvestment in construction, among other trends.

Moreover, some of the cities that saw their home prices skyrocket in the last decade are also the cities where incomes are lagging behind the most. This makes buying a house and getting a mortgage a double whammy, with potential homebuyers having to choose from a pool of increasingly expensive homes with a budget that can’t quite keep up. For instance, in North Las Vegas, home prices increased 75% more than incomes. Likewise, in four other cities, property prices went up more than 50% compared to income increases.

As for the most expensive markets, the median home in San Francisco is $1,239,415. Two other markets also crossed the $1 million threshold: Fremont and San Jose, both in California. In Fremont’s case, prices nearly doubled compared to 10 years ago. As a result, even with today’s low interest rates, buying the median home in these cities would still require a monthly mortgage payment between $4,000 and $5,000 — assuming that the homebuyer could afford the standard 20% down payment.

Homebuyers in Least Affordable Housing Market Would Need to Earn $43,567 More to Avoid Being Cost-Burdened

To buy a home stress-free and have a mortgage just under 30%, home buyers in nine of the 15 most unaffordable markets would need to earn at least $10,000 more in some of the most in-demand cities — and go as high as $43,567 more in San Francisco.

Although affordability seems more within reach in the six other unaffordable cities, homeowners there who want to cover their mortgage would still need to earn much more than they currently do: from $1,882 in Seattle to $6,506 in Boston.

The Most Affordable Housing Markets: In 6 Cities, Mortgages Take up Less Than 10% of Income

Detroit is the most affordable large U.S. city, with the average mortgage here taking up a meager 7% of the household income, down from 8% in 2010. Rounding out the top three are Cleveland and Toledo, OH, both of which boast mortgages that account for less than 10% of homeowners’ income. In all three cities, incomes have been increasing at a faster pace than home prices, with home prices in the two Ohio markets actually decreasing in the last decade.

And, while home price declines are not necessarily a good sign, a market that self-corrects or a city where incomes are not outrun by skyrocketing property values could offer residents a better chance at homeownership. The opposite of unaffordable markets, the U.S. cities where mortgages take up less than 30% of household income reflect the balanced conditions that most homebuyers and homeowners would welcome.

In 45 Markets Out of 100, Incomes Increased Faster Than Home Prices

From Seattle and Indianapolis — where the difference between home price changes and income changes is just 1% — to Cleveland, where home prices actually decreased in the last 10 years, some of these 45 cities give interested homebuyers real cause for hope.

Compared to the period between 2010 and 2015 — when home prices declined in no fewer than 19 markets — from 2010 to 2020, only two markets remained in this category: Cleveland and Toledo, OH. Here, household incomes went up 29% and 21%, respectively, while median home prices continued to scale down.

The table below contains more data points on income, home prices and mortgage affordability for the 100 largest U.S. cities included in the study, from the three years covered: 2020, 2015 and 2010. Use the tabs to see all the data and filter and rank the cities based on the categories you are interested in:

Methodology

- Study based on the 100 most populous cities in the U.S., sourced from the U.S. Census Bureau (2018). Population by age, American Community Survey 1-year estimates.

- The median income per household sourced from the U.S. Census Bureau (2010 and 2015). For the 2020 figures, we indexed the 2019 income using the national growth index from the average change index (4.5%) calculated by BEA.gov.

- The median home price per city sourced from the U.S. Census Bureau (2010 and 2015: ACS 1-Year Estimates, Detailed Tables by Owner-Occupied Housing Units). To calculate 2020 median home prices, we applied the metro growth index from NAR to 2019 city median sales prices.

- For this study an affordability ranking was created based on mortgage rate calculators and financial PMT function (which calculates the payment for a loan based on constant payments and a constant interest rate). The standard 20% down payment amount was calculated based on the median home price in each city. The interest rate we used is the most frequent, 30-year fixed rate mortgage average, with data from the last six months.

Fair use and redistribution

We encourage you and freely grant you permission to reuse, host, or repost the story in this article. When doing so, we only ask that you kindly attribute the authors by linking to Point2Homes.com or this page, so that your readers can learn more about this project, the research behind it and its methodology.