Mortgage affordability in Canada has eroded sharply in the past decade. In fact, in the last 10 years, the share of income needed to afford a mortgage has gone up exponentially, with monthly mortgage payments becoming a financial burden for increasing numbers of homeowners across the nation.

Exacerbating the problem, the COVID-19 pandemic forced homebuyers to completely rethink their needs and buying strategy. Demand for larger homes has been on the rise, while the building sector has been crippled by issues ranging from a scarce labour force to supply bottlenecks, pushing home prices to new heights.

But the pandemic-related disruptions and challenges are just the most recent events undermining ownership affordability in the country. As our latest housing affordability study shows, the increase in income is no match for the surging home prices in the 50 most populous Canadian cities. And the disparity between galloping home prices and slower-moving incomes means that the number of unaffordable cities (where homeowners spend more than 30% of their income to cover the mortgage alone) is going up at an alarming rate.

Here are the mortgage affordability study highlights:

- In the past decade, mortgage affordability worsened in 38 of the 50 largest Canadian housing markets.

- The number of unaffordable markets jumped from six to 16 in the last 10 years.

- Income increase is no match for home price growth: In 18 cities, home prices increased between 100% and 148%, whereas the most significant income gain was 53% in Edmonton, AB.

- Since 2010, the benchmark composite price crossed the $1 million mark in four cities: Richmond, Burnaby and Vancouver, BC and Oakville, ON.

- Homeowners in three of the most mortgage-burdened cities (Burnaby, Richmond and Oakville) would need to earn an additional $50,000 to cover their mortgage stress-free.

- At the other end of the spectrum, in the three most affordable housing markets (Halifax, NS; Windsor, ON; London, ON) mortgages take up a little more than 10% of owners’ income.

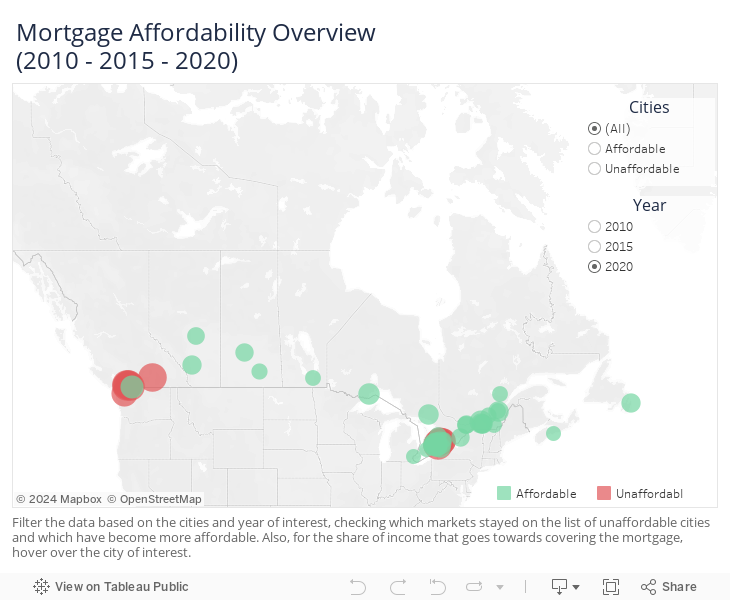

The Least Affordable Housing Markets: Since 2010, Number of Unaffordable Cities Jumped From 6 to 16

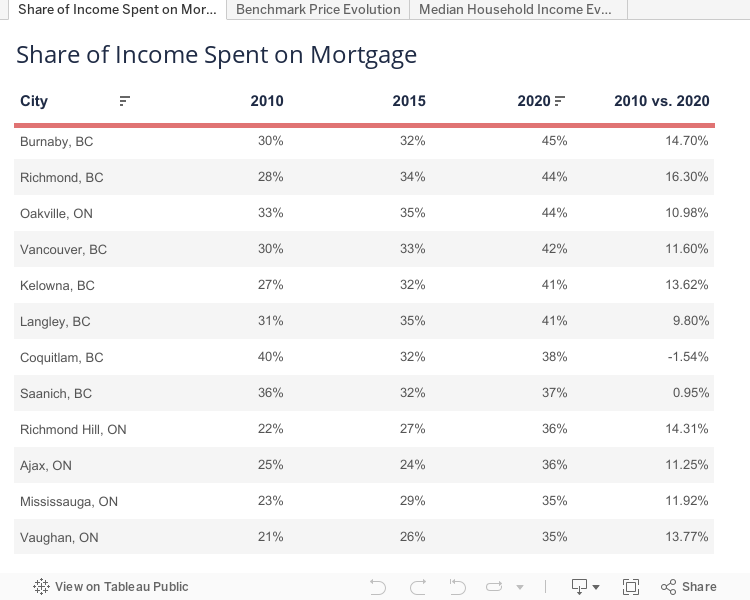

In 2010, only six of the cities included in our analysis were on the list of mortgage-burdened markets. And in fact, with half of them toeing the line between affordable and unaffordable, only three were in markedly unaffordable territory: Coquitlam, BC (40%), Saanich, BC (36.1%) and Oakville, ON (32.8%). By 2015, the number of cities where mortgages take up more than 30% of homeowners’ income grew to eight.

Fast forward to 2020 and the list is much longer. Moreover, with the least unaffordable market of the 16 taking up 32.2% of homeowners’ median income, all of them are firmly positioned in mortgage-burdened territory.

Meanwhile, none of the cities that were on the unaffordable list in 2010 disappeared from it by 2020. But two cities set the opposite record: in Richmond, BC and Kelowna, BC, mortgages took up around 27% of income in 2010. Now, 10 years later, monthly mortgage payments represent more than 40% of household income, placing the two cities among the top five most cost-burdened in the country.

3 Cities See More Than 100% Gap Between Income Growth & Home Price Growth

Although not all of them became unaffordable, a total of 38 cities experienced deteriorating mortgage affordability due to the widening gap between the growth of home prices and incomes. Home prices are increasing much faster than wages, causing affordability to erode despite mortgage rates remaining at record lows. For instance, of the 50 cities included in the study, 18 markets have seen home prices more than double in the last decade, with Kitchener, ON (148% increase), Abbotsford, BC (132%) and St. John’s, NL (125%) leading the way.

Incomes not only didn’t keep the pace, but in some cities, wage growth is far behind home price growth. The city with the most significant household income increase is Edmonton, AB. Here, incomes are 53% higher compared to 2010. The other 49 cities included in the study have seen much more modest wage growth, ranging between 11% and 49%.

Homebuyers in 3 Least Affordable Cities Would Need to Earn $50,000+ More to Avoid Being Mortgage-Burdened

So how much more money would homeowners in the most unaffordable cities need to earn in order to avoid being burdened by their monthly mortgage payments? To buy a home stress-free and have a mortgage just under 30%, homeowners in three of the 16 most unaffordable markets would need to make at least $50,000 more. In particular, in Burnaby, BC, Richmond, BC and Oakville, ON, owners would need to earn an extra $54,429, $55,317 and $51,307, respectively.

And although affordability seems more within reach in the 13 other unaffordable cities, homeowners there who want to cover their mortgage would still need to earn much more than they currently do — from $12,675 and $16,333 more in Surrey, BC and Whitby, ON, to $45,865 in Vancouver, BC respectively.

The Most Affordable Housing Markets: In 10 Cities, Mortgages Take Up Less Than 15% of Income

Conversely, Halifax, NS, is the most affordable city of the 50 markets in the study. The average mortgage here takes up 10.8% of the median household income, down from 12.5% in 2015. Rounding out the top three are Windsor, ON and London, ON, both of which boast mortgages accounting for less than 12% of homeowners’ income. In all three cities, incomes have been increasing at a faster pace than home prices in the last decade.

In fact, with the exception of Oshawa, ON, incomes in all 10 of the most affordable housing markets have increased faster than home prices. And, although not as affordable as the top 10, cities like Edmonton, AB and Burlington, ON have also recorded faster income growth compared to home price increases. The only unaffordable city where household incomes went up at a faster pace than home prices is Coquitlam, BC.

The table below contains more data points for the 50 most populous Canadian cities included in the study. Use the three tabs above the table to see all the data and filter and rank the 50 cities based on the categories you’re interested in:

Methodology

- This study is based on the 50 most populous cities in Canada, sourced from Statistics Canada (Census Profile, 2016).

- The real median household income after tax from 2006 to 2018 was sourced from owners’ data from the Canada Mortgage and Housing Corporation. For the 2020 figures, we indexed each income with the weekly salary increase from 2018 to December 2020, with the exception of the following, which were indexed by region and province salary changes: Mississauga, Brampton, Surrey, Laval, Markham, Vaughan, Longueuil, Burnaby, Richmond, Richmond Hill, Oakville, Burlington, Lévis, Barrie, Coquitlam, St. Catharines, Guelph, Cambridge, Whitby, Kelowna, Ajax, Langley, Saanich, Terrebonne, Milton, St. John’s. This data is based on Statistics Canada, the Canadian Income Survey 2012-2018, the Survey of Labour and Income Dynamics 2006-2011.

- Home prices were calculated based on CREA HPI and the benchmark composite prices from January 2010 to November 2020. For Fraser Valley cities we used 12-month, 2020 averages for detached homes, via fvreb.bc.ca. Local MLS medians where used for Burlington, Barrie, Oshawa, Richmond Hill (via listing.ca) and Coquitlam (via rebgv.org). For the following cities, we used metro region home prices, as local figures were not available: Burnaby, BC, Brampton, ON and London, ON.

- For this study an affordability ranking was created based on mortgage rate calculators and financial PMT function (which calculates the payment for a loan based on constant payments and a constant interest rate). The standard 20% down payment amount was calculated based on the benchmark composite home price in each city. The mortgage rate used was based on monthly payment at a five-year fixed interest rate of 2.5% amortized over 25 years, per the standard of RBC.

Fair use and redistribution

We encourage you and freely grant you permission to reuse, host, or repost the story in this article. When doing so, we only ask that you kindly attribute the authors by linking to Point2Homes.com or this page, so that your readers can learn more about this project, the research behind it and its methodology.